Discussing Annuities and Retirement Income

Annuities are products uniquely designed to deliver a steady stream of retirement income clients can’t outlive. However, persistent misconceptions about annuities prevent some clients and advisors from even considering these products in a retirement plan.

“Annuities are too complex and expensive.”

“Savings and investments will generate enough income for retirement.”

“Annuities require turning over assets to an insurance company, irrevocably.”

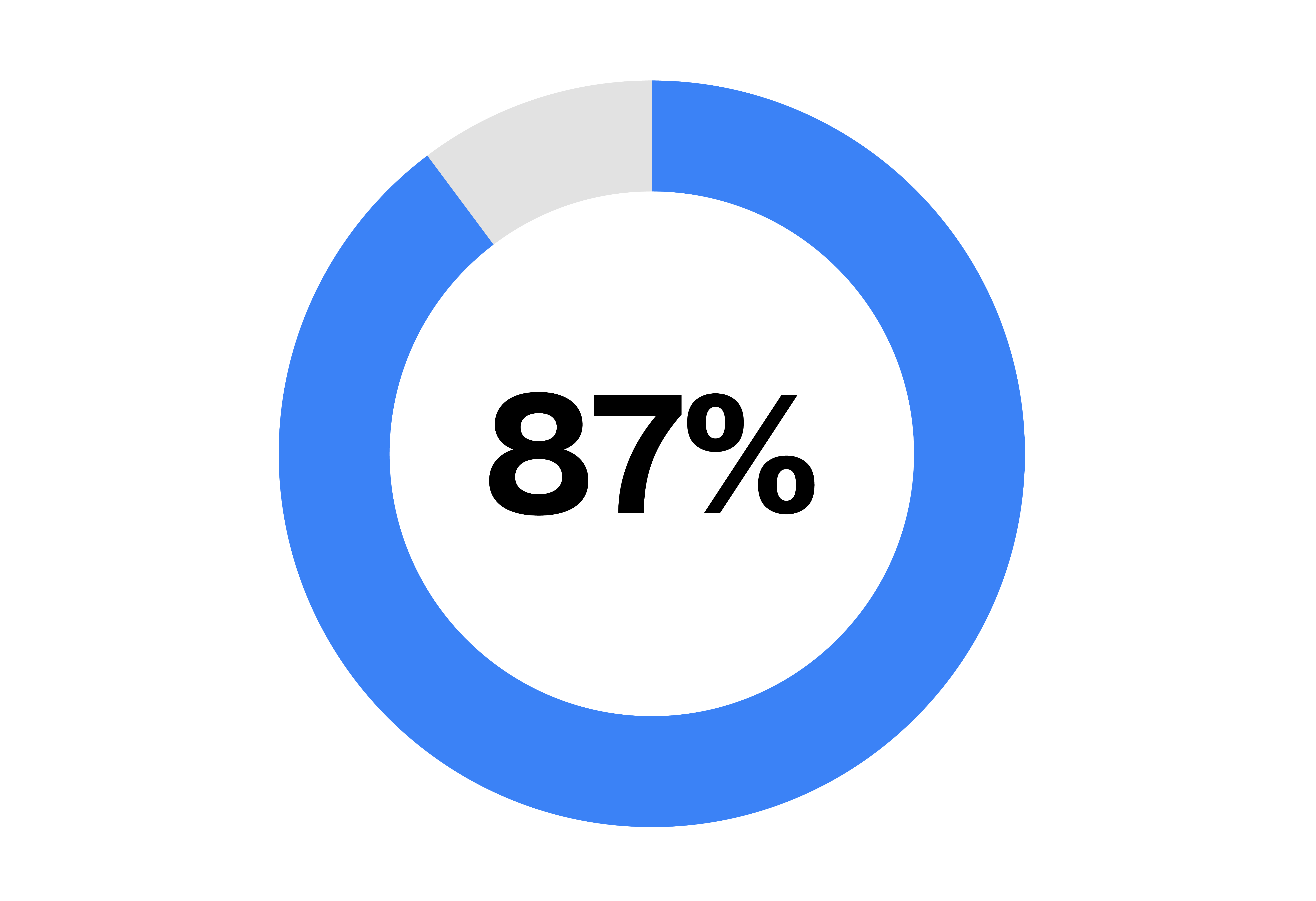

Even the word “annuity” carries a stigma for some. Research shows clients want what these products provide: principal protection and guaranteed income. The Insured Retirement Institute reports that 87% of retirees are likely to buy an annuity when described by its features. But when an annuity is described by name, the likelihood of purchase drops to 45%.1

As your clients approach retirement, it’s important to discuss their retirement income plan and ensure they are comfortable with the strategy and solutions you propose. This conversation guide provides insights into retirement planning challenges, clients’ fears, and ways modern annuities can be used to deliver secure income and peace of mind many clients want. It can be used to enrich your retirement planning conversations.

New Retirement Realities

Planning for a secure retirement isn’t as straightforward as it used to be. Retirements are expanding. People are living longer. Improvements in healthcare, personal wellness, and medicine are contributing to longer lifespans. In fact, the number of Americans living to age 100 is projected to quadruple by the 2050s. Likewise, people often retire earlier than planned.2

And the reliable retirement funding sources Americans relied on 50 years ago simply aren’t available today. Employer-provided pensions are largely a thing of the past, and the long-term outlook for Social Security is uncertain. Fixed income investments like bonds—once a stalwart producer of safe income in a retiree’s portfolio—can’t provide sufficient income for most retirements.

Clients today need a retirement income strategy that takes these realities into account, so they feel confident their plan will support them for 30 or even 40 years and can see it through to the end.

“We consistently see that those who plan for longevity feel more confident about retirement. The key drivers of that confidence? Working with an advisor, having access to guaranteed income, and building a plan that’s designed to last.”

— Michael Finke | Professor of Wealth Management & Frank M. Engle Distinguished Chair in Economic Security, American College of Financial Services

Addressing Common Risks

When discussing possible income strategies, it’s important for clients to understand the risks that can derail their retirement plans.

Two of the greatest risks are longevity risk and sequence of returns risk.

Longevity risk: A retiree outlives their retirement income and cannot fund their living expenses.

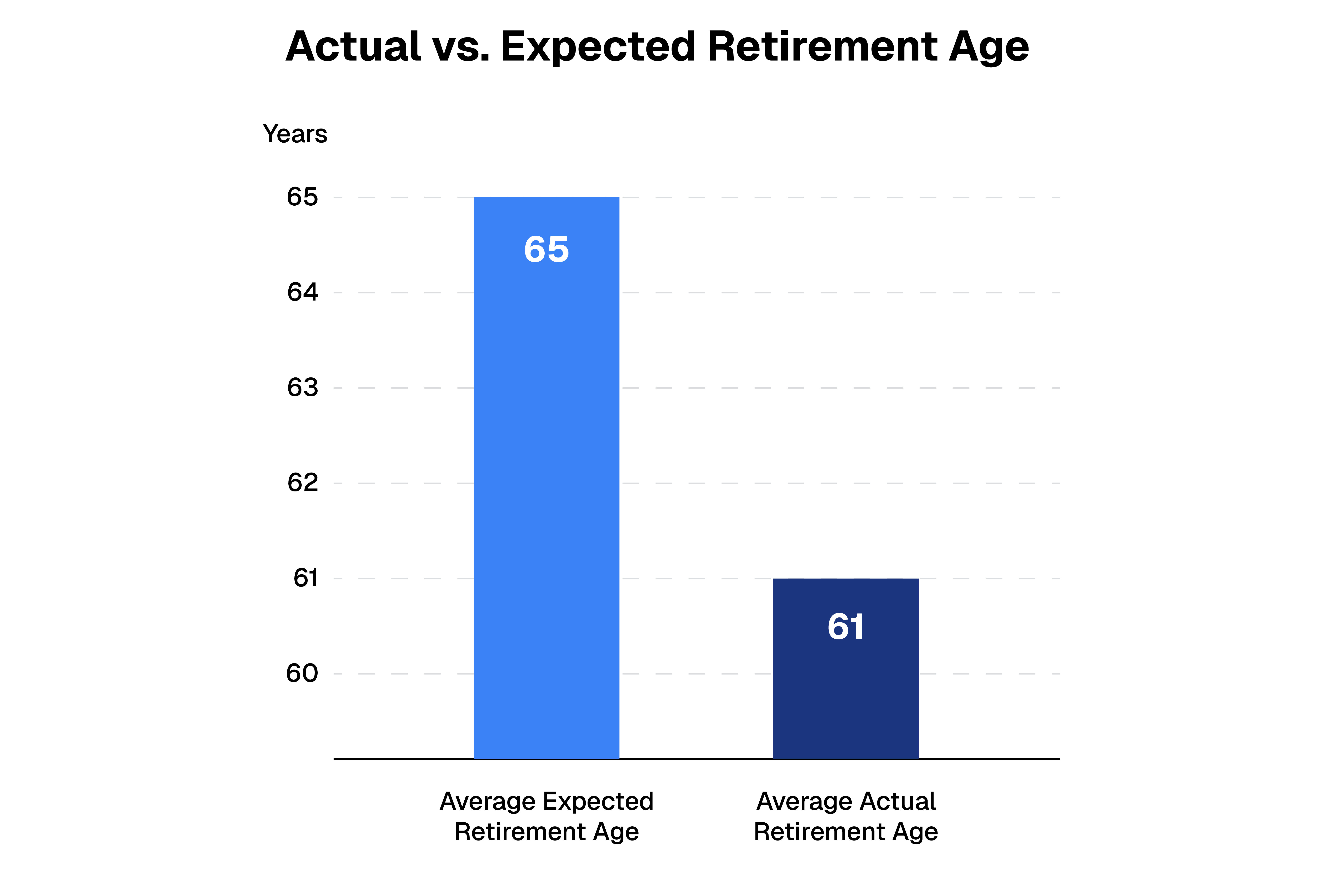

Here is an example of what living longer can mean for your income requirements: A 65-year-old living 14 years to age 79 would need $854,000 in income to meet his or her expenses. By living an additional four years to age 83, the total retirement income need increases to $1,170,000 — 37% higher — assuming 3% inflation.5

Sequence of returns risk: A market downturn just before or soon after retirement depletes a portfolio to the degree it is unable to support income withdrawals.

Overspending early in retirement also presents a significant risk, potentially stressing a portfolio and reducing future income.

A well-thought-out retirement strategy helps ensure retirees have enough protected income to cover at least their essential expenses for their entire lives, regardless of how long they live.

The Role of Guaranteed Income

A retirement portfolio incorporating an annuity can offer clients several benefits:

• A predictable stream of pension-like income they can’t outlive

• Peace of mind during unsettling periods of market volatility

• Confidence to stay the course with their financial plan

An annuity can make great sense for clients who are not comfortable taking on more portfolio risk to generate income, or fear outliving their savings. They want a source of contractually guaranteed income they can count on for the length of their retirement, which an annuity provides.

How Annuities Have Changed

Many leading insurance carriers now offer fee-based annuities designed to reduce costs and deliver greater value, flexibility, and transparency. These products can be used strategically in financial plans to mitigate risk, add a measure of principal protection, and create a predictable stream of secure income to help fund essential expenses in retirement.

Clients today have access to a wide range of low-cost, commission-free annuities built to protect and grow their retirement savings. Many commission-free annuities come without surrender (or lock-up) periods and have lower fees and greater accumulation potential than their commissioned counterparts. If your client owns a commissioned annuity, you can compare the existing product to commission-free options to see if your client’s costs can be lowered and benefits improved.

Impacts on the Financial Plan: Where to Start

Annuities provide two highly sought after qualities for retirement planning: versatility and predictability. Many investors use annuities to meet their necessary monthly expenses in retirement, like a mortgage, food, healthcare and other “must-haves.”

An annuity can act as a personal pension to help ensure essential retirement expenses are covered.

With essential expenses covered by income from the annuity, the client and advisor have the flexibility to invest the remainder of the portfolio for growth to fund discretionary spending.

Annuities are uniquely designed to provide guaranteed lifetime income for retirement. Incorporating guaranteed income from an annuity can give clients confidence their needs in retirement will be met while giving them freedom to invest remaining portfolio assets for legacy or other goals.

Annuities for Income: What the Academics Say

While annuities may be controversial in some circles, they are not among academics. Prominent retirement experts underscore both the financial and psychological benefits of annuities in support of their use in retirement portfolios. Many argue that annuities, through their structure, manage risks and bring efficiencies to income that simply cannot be achieved through investments alone.

Next Steps

Annuities are powerful tools uniquely designed to generate guaranteed income for retirement. Commission-free annuities offer lower costs, greater transparency, and improved benefits and are easily accessible to advisors and clients today.

There are many types of annuities, and it’s important for you and your client to determine if an annuity is a smart choice for their retirement income plan and which product is right for them. Show your client the financial plan with and without an annuity. It’s a great way for them to see the potential impact and make a decision that aligns with their financial and psychological needs.

To find annuity solutions that best meet your clients’ needs, use DPL’s Product Discovery Tools. Available through your DPL Advisor Dashboard, these tools make it easy to compare products, generate proposals, and have productive conversations about annuities, income and protection with clients.

[press-a-contact-location]

Sources:

1 Insured Retirement Institute. “Aligning Retirement Expectations with Financial Resources.” March 10, 2022.

2 Pew Research Center. “U.S. centenarian population is projected to quadruple over the next 30 years.” Jan. 9, 2024

3 Morningstar

4 “Retirement Longevity Planning: An Expert’s Perspective.” Michael Finke, May 13, 2025

5 Insured Retirement Institute Fact Book 2023

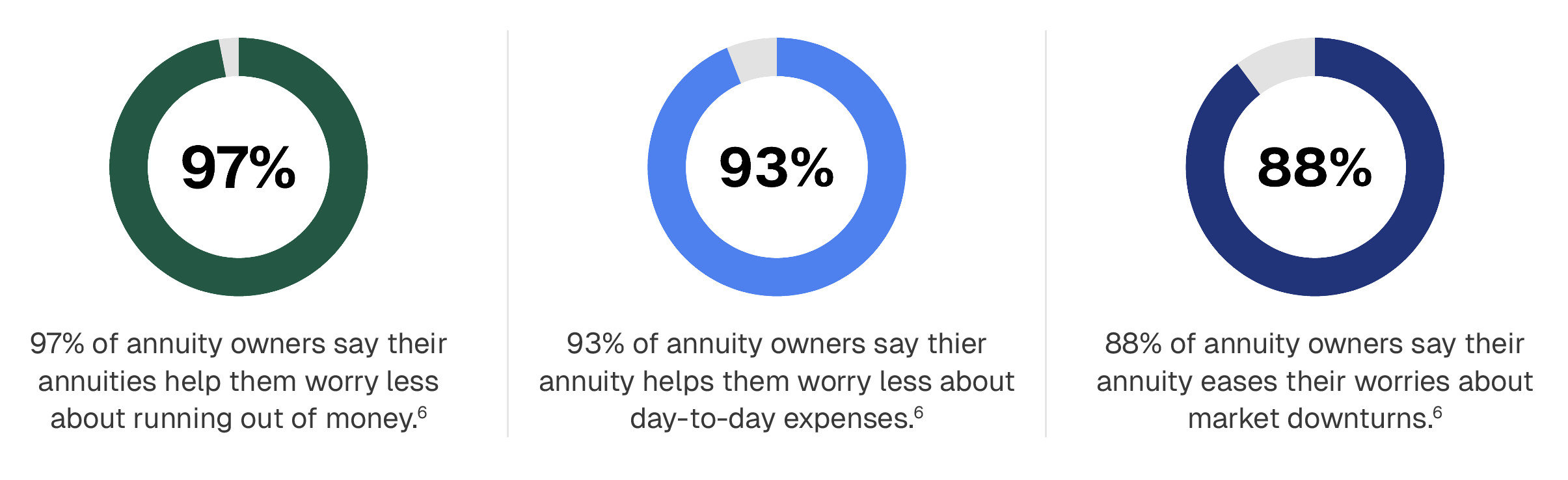

6 BlackRock, “Annuity owners value the benefits of lifetime income.” October 22, 2024.

Disclosures:

Guarantees are based on the claims paying ability of the insurance carrier issuing the product.

• Not a deposit • Not FDIC or NCUSIF insured • Not guaranteed by the institution • Not insured by any federal government agency • May lose value

When evaluating the purchase of a variable annuity, you should be aware that variable annuities are long-term investment vehicles designed for retirement purposes and will fluctuate in value; annuities have limitations; and investing involves market risk, including possible loss of principal.

The general distributor for variable products is Johnstone Brokerage Services ("JBS"), member FINRA/SIPC 117 San Augustine Street, Center TX 75935. JBS is wholly owned by DPL Financial Partners.

Fixed index annuities are not stock market investments and do not directly participate in any equity, bond, other security, or commodities investments. Unless stated otherwise, market Indices do not include dividends paid on the underlying stocks, and therefore do not reflect the total return of the underlying stocks; neither an index nor any market index annuity is comparable to a direct investment in the equity markets. Clients who purchase index annuities are not directly investing in a stock market index.

This material is not a recommendation to buy or sell a financial product or to adopt an investment strategy. Investors should discuss their specific situation with their financial professional.

© 2025 DPL Financial Partners, LLC. All rights reserved