Multi-Year Guaranteed Annuity (MYGA)

A multi-year guaranteed annuity (MYGA) is a type of fixed annuity offering a tax-deferred guaranteed rate of return over a duration from two to ten years.

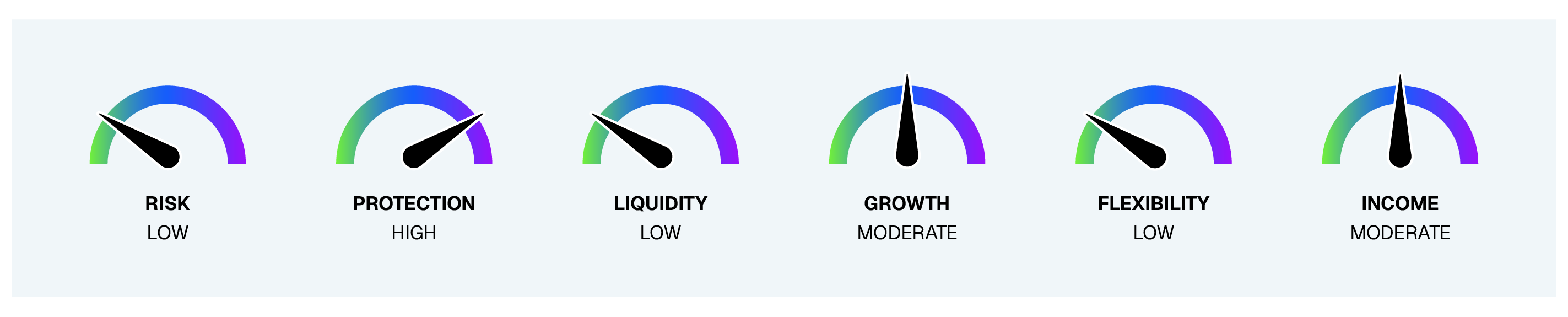

Multi-Year Guaranteed Annuity (MYGA)

Client Risk Profile: Low

Protection Level: High

Funding Source: Cash, CDs, Fixed Income

Similar to a certificate of deposit (CD) or money market funds, a multi-year guaranteed annuity, or MYGA, offers complete downside protection against market fluctuations by guaranteeing a minimum rate of return for the duration of the investment. However, unlike CDs or money market funds, interest rates often are higher and assets grow tax deferred, allowing the possibility of greater accumulation over the life of the annuity. These simple, short-duration annuities, ranging from two to ten years, often are used by advisors as fixed income allocations.

Consider a MYGA when your client needs:

Principal Protection: MYGAs are typically used for clients nearing or in retirement, as they protect principal from market downturns, yet provide a minimum guaranteed rate of return.

Fixed Income: MYGAs provide a consistent stream of income for clients that are looking to de-risk their portfolios from equities.

Cash Replacement: MYGAs can be used instead of cash investments, such as CDs or money market funds, to help generate better returns subject to the terms of the contract.

Disclosures:

Surrender charges, market value adjustments and other contract charges may apply that can reduce the principal.

Guarantees are backed by the financial strength and claims paying ability of the issuing insurance company.

There are risks, fees and charges associated with fixed annuities.

The purchase of an annuity within a retirement plan that already provides tax deferral under sections of the Internal Revenue Code results in no additional tax benefits. An annuity should be used to fund a qualified plan based upon the annuity’s features other than tax deferral. All annuity features, risks, limitations, and costs should be considered prior to recommending the purchase of an annuity within a tax-qualified retirement plan. In addition to surrender charges, withdrawals are subject to income tax.

Withdrawals prior to age 59 1/2 may also be subject to a 10% federal tax penalty.

Contact Us

Have more questions about our insurance offering? Call us at 888.327.0049 to speak to a DPL Consultant.