As Record Number of Baby Boomers Near Retirement Age, Concerns Around Savings Grow

It is estimated more Americans will turn 65 in 2025 than any other year in history.2 With more Baby Boomers approaching retirement age, it appears the desire for financial security in retirement is fueling an interest in annuities. U.S. annuity sales skyrocketed to their highest levels yet in the first half of the year, reaching $223 billion, as consumers and financial advisors turn to these products for guaranteed income.3

Increasing fears around retirement savings

The number of people entering retirement age is growing at the fastest pace ever, with more than 4.1 million Americans turning 65 each year through 2027, according to the Alliance for Lifetime Income’s Protected Retirement Income and Planning (PRIP) survey. As the number of retirees increases, so does their concern around putting away sufficient savings to last through retirement years.

Also growing: the retirement gap. The difference between estimated retirement expenses and projected retirement income is getting larger as individuals live longer and want to maintain their lifestyle even as inflation and common retirement costs like healthcare climb. The latest research puts the magic number most individuals believe they will need to comfortably retire just north of $1 million.4 However, most Americans have far to go before reaching that amount in savings.

As a result of the increasing gap, many are feeling a sense of heightened stress about their financial security. The PRIP survey found:

- Nearly half of retirees have anxiety about spending money in retirement

- 54% of pre-retirees worry about outliving their savings, and 42% said outliving their savings was “top of mind”

Respondents ages 45-75 listed various economic reasons for their retirement fears:

- Two-thirds cited inflation as a top concern

- 60% of respondents listed healthcare costs as a top concern

- Over half are worried about Social Security reductions

Many are taking precautionary measures to ensure they don’t outlive their savings—33% of Americans approaching retirement say they’re considering delaying it altogether according to the survey.

More advisors, investors turn to annuities

Financial advisors have been hearing their clients’ concerns about insufficient income in retirement, and a growing number are incorporating annuity products into their clients’ portfolios.

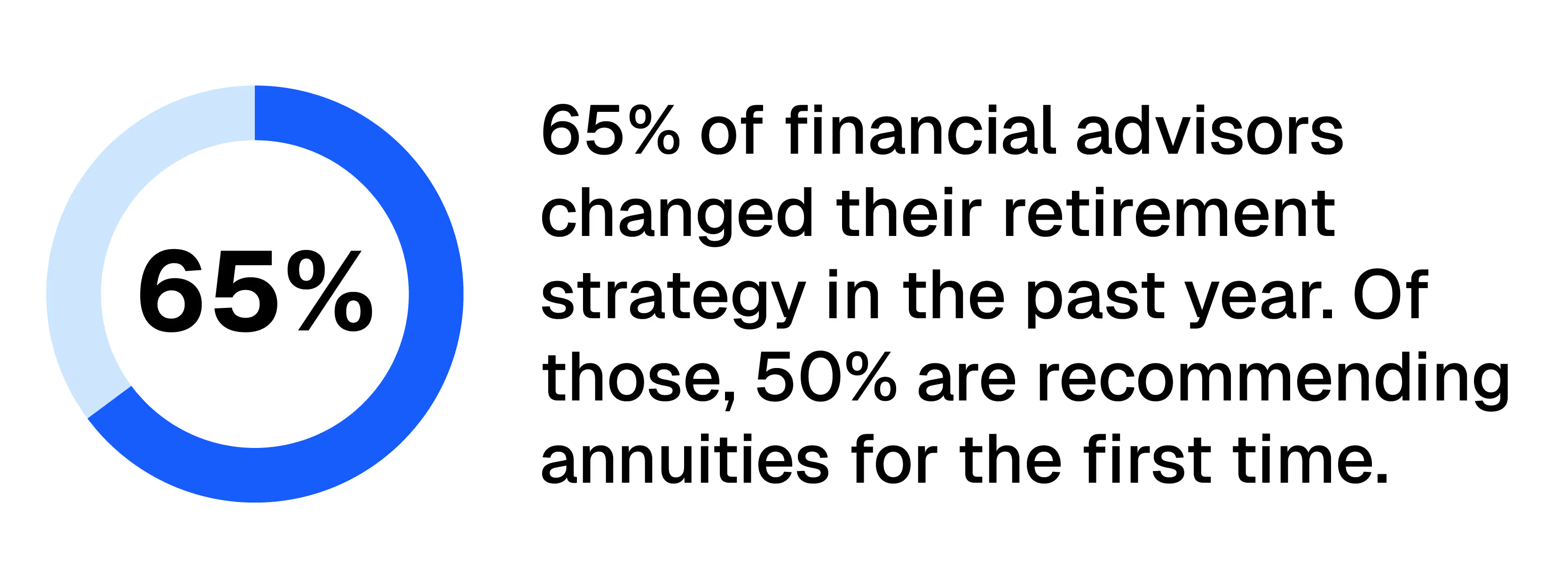

The PRIP survey found that 65% of financial advisors surveyed said they have altered their retirement planning strategy in the past year—with half of them recommending annuities for the first time. This indicates a move away from traditional retirement planning, further emphasized by the fact that 30% of advisors decreased exposure to stocks. Only 30% of advisors said they are investing more client money in stocks and just over a third said they put more client money into US Treasurys.

Consumers also recognize the benefits of annuities. Of those surveyed, 64% of consumers ages 45 to 75 said they would put money into an annuity versus the stock market in the event of receiving a $100,000 windfall.

Data from Life Insurance Marketing and Research Association supports these findings. According to LIMRA, second quarter annuity sales reached $116.6 billion, the highest quarterly total ever recorded.5

Annuities and guaranteed income

The PRIP survey found that 95% of near retirees surveyed listed “income protection” as important to their retirement plans. Annuities can mitigate longevity risk, while also serving as efficient income generators. Annuities can outperform fixed income and provide payouts long after fixed income portfolios would be exhausted. In addition, modern, commission-free annuities can unlock greater consumer value by offering significantly lower costs and improved benefits than traditional annuities.

By providing a secure income source throughout retirement, they can help investors mitigate market volatility, ease their fear of outliving their savings, and ensure that essential expenses like health care and housing are covered.

[press-a-contact-location]

- Life Insurance Marketing and Research Association (LIMRA). "U.S. annuity sales set a new record in first half of 2025. July 28, 2025

- Alliance for Lifetime Income. "2025 Protected Retirement Income and Planning Survey. July 9, 2025

- LIMRA. op. Cited July 28, 2025

- https://news.northwesternmutual.com/planning-and-progress-study-2025

- LIMRA. op. Cited July 28, 2025.

Guarantees are based on the claims paying ability of the issuing insurance company.

.avif)