What is an Annuity and How Does it Work?

.avif)

An annuity is an insurance product designed to provide guaranteed lifetime income. Just as you insure your life, home and vehicle, annuities insure against the risk of outliving your retirement savings.

Certain annuities can also be used to protect assets against market volatility or grow wealth prior to retirement. Think of an annuity as a personal pension that provides a paycheck, every month in retirement, for as long as you live.

How Annuities Work

When you purchase an annuity, you make a lump-sum payment or a series of payments to an insurance company. The insurance company then invests your money and, when you want to begin receiving income, pays you a steady stream of income that can start immediately or many years later, depending on your needs.

Annuities operate in two main phases:

- Accumulation phase: During this initial phase, your money grows tax-deferred within the annuity. The insurance company invests your funds based on the type of annuity you have chosen, allowing your money to grow over time.

- Payout phase: When you're ready to start receiving income, you enter the payout phase. This is when the accumulated value of your annuity is turned into a stream of income payments. You can select from various payout options, such as receiving flat or rising income for a set number of years or until your death.

The amount of income you receive from an annuity will depend on the type of annuity you choose, the amount of money you put into the product, how long you wait to start payments, and demographic details such as your age.

Expert Perspective: Wade Pfau on Annuities

In his podcast, Retire with Style, retirement researcher Wade Pfau addresses the confusion around annuities as investments.

"Generally speaking, we're thinking about annuities for insurance protections in the frame of retirement income, not as an investment,” Pfau says. “When you're facing longevity risk and want to have a sustainable, predictable income in retirement, that's where you think about the annuity.”

Types of Annuities

Annuities come in many different forms, each with its own features and benefits. Three common types of annuities include:

- Fixed annuities: A fixed annuity is a straightforward product, like a CD. In a fixed annuity, your money is invested in conservative, low-risk assets such as bonds or fixed-income securities. The insurance company pays a guaranteed fixed interest rate on your money, providing you with a predictable return over the agreed-upon term

- Variable annuities: Variable annuities offer a range of investment options. Your returns are dependent on the performance of these underlying investments, which means you can potentially earn higher returns than on fixed annuities, but there also is the potential for you to lose money in a market downturn

- Fixed index annuities: Fixed index annuities combine elements of fixed and variable annuities. The returns are linked to the performance of a specific stock market index, like the S&P 500, providing the potential for higher returns compared to fixed annuities, while offering complete downside protection so you don’t lose money when the market goes down.

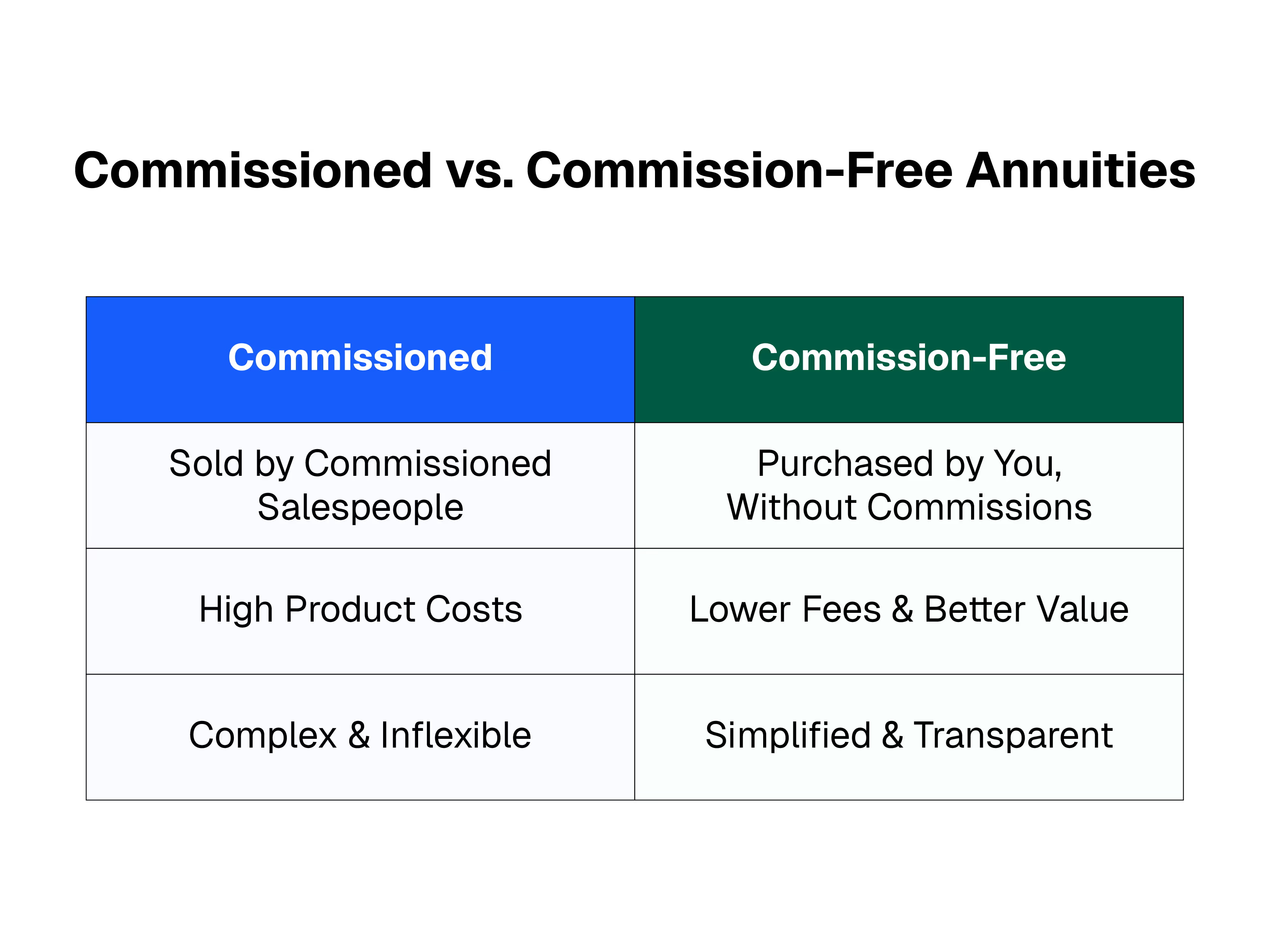

Modern vs. Conventional Annuities

Conventional annuities come with hefty sales commissions built into the products. These commissions can drive up your costs, limit earning potential and reduce lifetime income benefits.

In contrast, modern annuities are commission-free (also known as fee-based or no-load annuities). These simplified products are built to deliver better consumer value with lower costs, improved benefits, and a buying experience you control.

Annuity Pros

Annuities offer many advantages that make them appealing to individuals seeking a measure of certainty in their financial plan:

- Guaranteed income: Annuities can provide a secure income stream, ensuring you have a reliable source of funds to cover essential expenses during retirement

- Tax advantages: Annuities offer tax-deferred growth, which means you aren’t taxed on the interest you earn while your money is in the annuity. You don’t pay taxes until you begin taking income payments, which can help your retirement savings grow faster

- Flexibility: Annuities can be customized to fit your specific needs. You can choose the type of annuity, the amount of money you want to put into the annuity, your income start date, whether you want any remaining funds distributed to a beneficiary or charity, and more

Risks and Considerations

Some things to consider as you explore annuities:

- Fees and expenses: Some annuities have fees associated with certain features and benefits, so it is important to understand the total cost of the product you are purchasing

- Complexity: Some types of annuities are more complex than others, so you’ll want to consult with a fiduciary financial advisor if you feel you don’t understand the product you are purchasing

- Liquidity: Many modern annuities enable you to access some of your money without paying a penalty (or “surrender”) fee. Others do not. Do not purchase an annuity until you understand and are comfortable with your access to the money you put into the product

Annuities can be valuable retirement planning tools — even more so now that they are available commission-free — without some of the steep embedded sales fees that have historically contributed to the high cost and complexity of conventional annuities.

There are many types of annuities. Some are geared toward building wealth and protecting against market losses, while others are more focused on delivering guaranteed income.

There are annuities that offer attractive rates of return when used as alternatives to CDs and savings accounts.

Other annuities give you the opportunity to participate in a market index, like the S&P 500, to potentially grow your money more quickly while offering some protection from market downturns.

In addition, annuities can be customized to meet specific needs by adding contract provisions called “riders.” For example, there are riders to help offset the cost of long-term personal care, ensure your income payments keep pace with inflation, or stipulate that any principal remaining in the contract is paid to a beneficiary if the owner dies before the full value of the annuity has been paid out.

The most important thing when considering an annuity is that you fully understand the product you're buying, including its features and costs.

DPL has several tools to help you learn more about commission-free annuities and see how these solutions fit in a retirement portfolio.

[press-a-contact-location]