Could Your Annuity Be Doing More for You?

Much like the smartphone category, the market for annuities is continuously evolving.

Over the past few years, the market has changed in significant ways:

- Rising interest rates have increased the levels of guaranteed income available through many annuities

- Newer annuity structures have made it possible for annuity owners to participate in stock market performance with no — or limited — downside risk

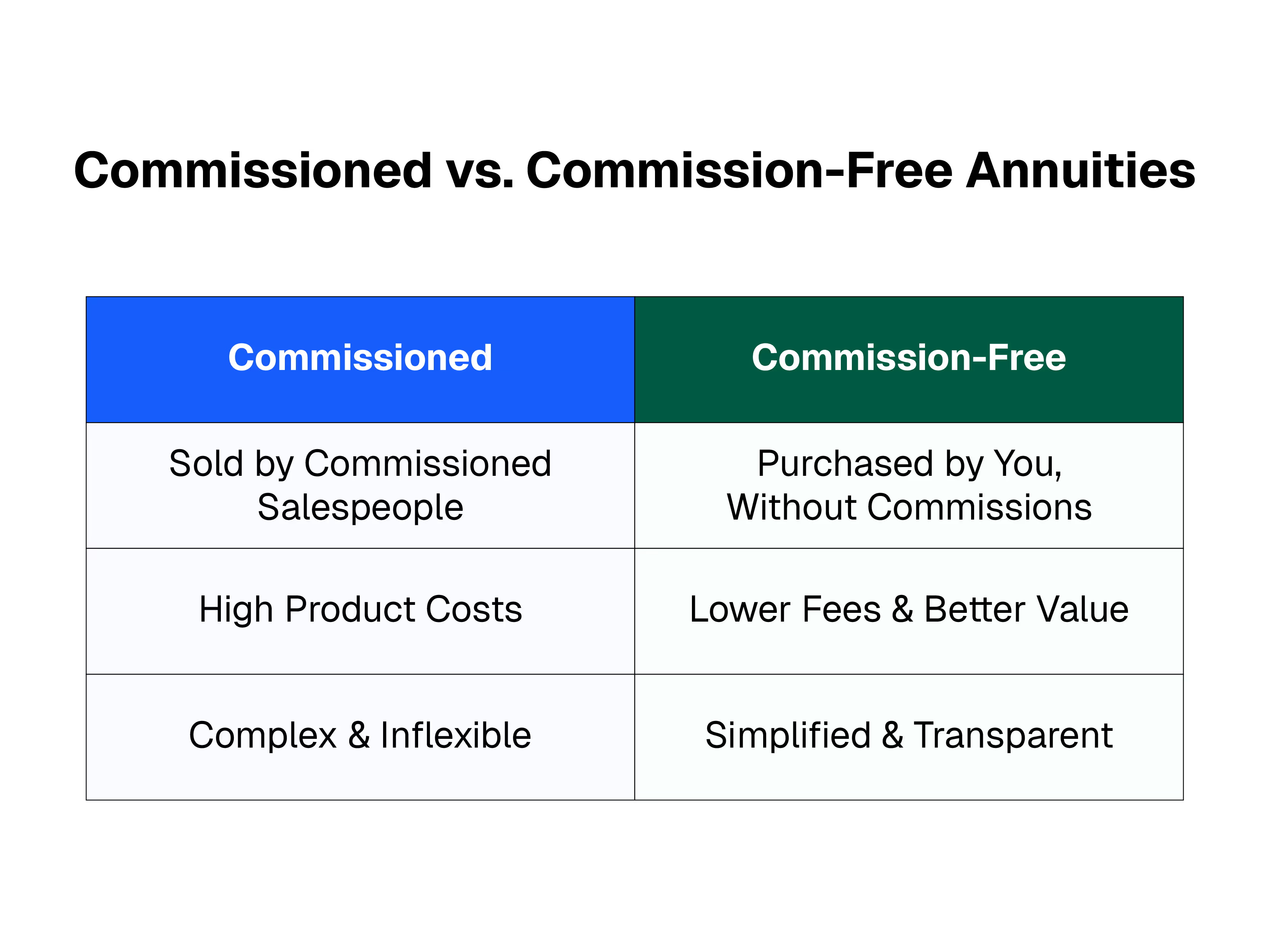

- Commission-free annuities have become widely available, offering significantly lower costs and improved benefits

As a result of these advances, some annuity owners are finding it beneficial to exchange an older annuity for newer options.

Three Reasons to Exchange an Annuity

Exchanging an older annuity for a newer, commission-free product can be a savvy financial move, often accomplished without negative tax consequences. Reasons to consider an exchange include:

- Increasing retirement income

One reason people purchase annuities is to secure a stream of guaranteed income for retirement. As interest rates have moved higher, so has the level of income generally offered by annuities. It’s possible that a new annuity will provide you with more income than an older one does.

- Extending income beyond your lifetime

Another reason to consider an exchange is to extend the guaranteed income period. For example, your current annuity may provide income over your lifetime, but not that of your spouse. Moving into a newer commission-free annuity makes it possible to guarantee income over both lifetimes.

- Evolving financial goals

Annuities may not be the only thing that has changed over the past decade. Your financial goals may be different today than they were years ago. For instance, you may decide to use the assets in your annuity to build a legacy rather than to provide retirement income. Often, building a legacy means maximizing growth. An annuity exchange might help in two ways. First, moving to a commission-free annuity could enhance growth by lowering overall costs. Second, modern annuity structures may offer better potential for growth than your current annuity does.

Benefits of an Annuity Exchange

If you’ve owned an annuity for several years, chances are it’s a variable annuity.

Comparing annuities to find products that best meet your needs has never been easier. The DPL Financial Partners platform offers an Annuity Comparison Calculator that can help determine whether your old variable annuity still makes sense for your portfolio, or if there is an alternative commission-free product that can provide greater transparency and value, and better alignment with your financial goals.

DPL’s comparison tool will ask how much income you need, or how much you need to invest to generate income, then will show you exactly how much income you can get and what that income will cost. It even shows you a side-by-side comparison of your current annuity to the recommended alternative, allowing you to see how costs and benefits compare.

Check Out The Annuity Comparison Calculator

All you need is a recent statement and a goal for the annuity, which could be guaranteed income, growth, or protected growth. With a few inputs, the calculator returns a side-by-side comparison of your current annuity to alternatives that best meet your goals. For other types of annuities, work with your advisor or a DPL Consultant who can assist with a review.

What is a 1035 Exchange?

If exchanging an existing annuity for a newer one could be advantageous, consider a 1035 exchange. This is a provision in the IRS tax code that allows for tax-free transfers of certain insurance products, including annuities. Through a 1035 exchange, you can reallocate assets directly from one annuity to another and maintain their tax-deferred status. That means you keep more money working for you. Your advisor or consultant can help you complete a 1035 exchange.

"Commission-Free Annuities Offer Greater Value, Transparency, and Alignment with Goals Than Older Products"

If you own an older annuity, it may be time for an upgrade to a modern product with potentially lower costs and improved benefits.

We can help you easily compare your annuity to a marketplace of low-cost, commission-free options.

[press-a-contact-location]

.avif)