Earn More, Worry Less: Your Guide to Multi-Year Guaranteed Annuities

Want to earn more on your savings while you worry less about market volatility? Multi-year guaranteed annuities (MYGAs) are the insurance industry’s alternative to bank certificates of deposit, or CDs. A good option for investors who prioritize security over high-risk, high-reward strategies, commission-free MYGAs offer a reliable way to protect and grow funds with limited exposure to market losses due to volatility.

"MYGAs provide a Secure, reliable, and tax-advantaged way to grow your retirement savings, offering the peace of mind that comes with a guaranteed return"

Because MYGAs are commission-free products, they can be easily incorporated into a retirement plan when you're working with a financial advisor.

Three key benefits MYGAs offer:

Earn greater guaranteed returns

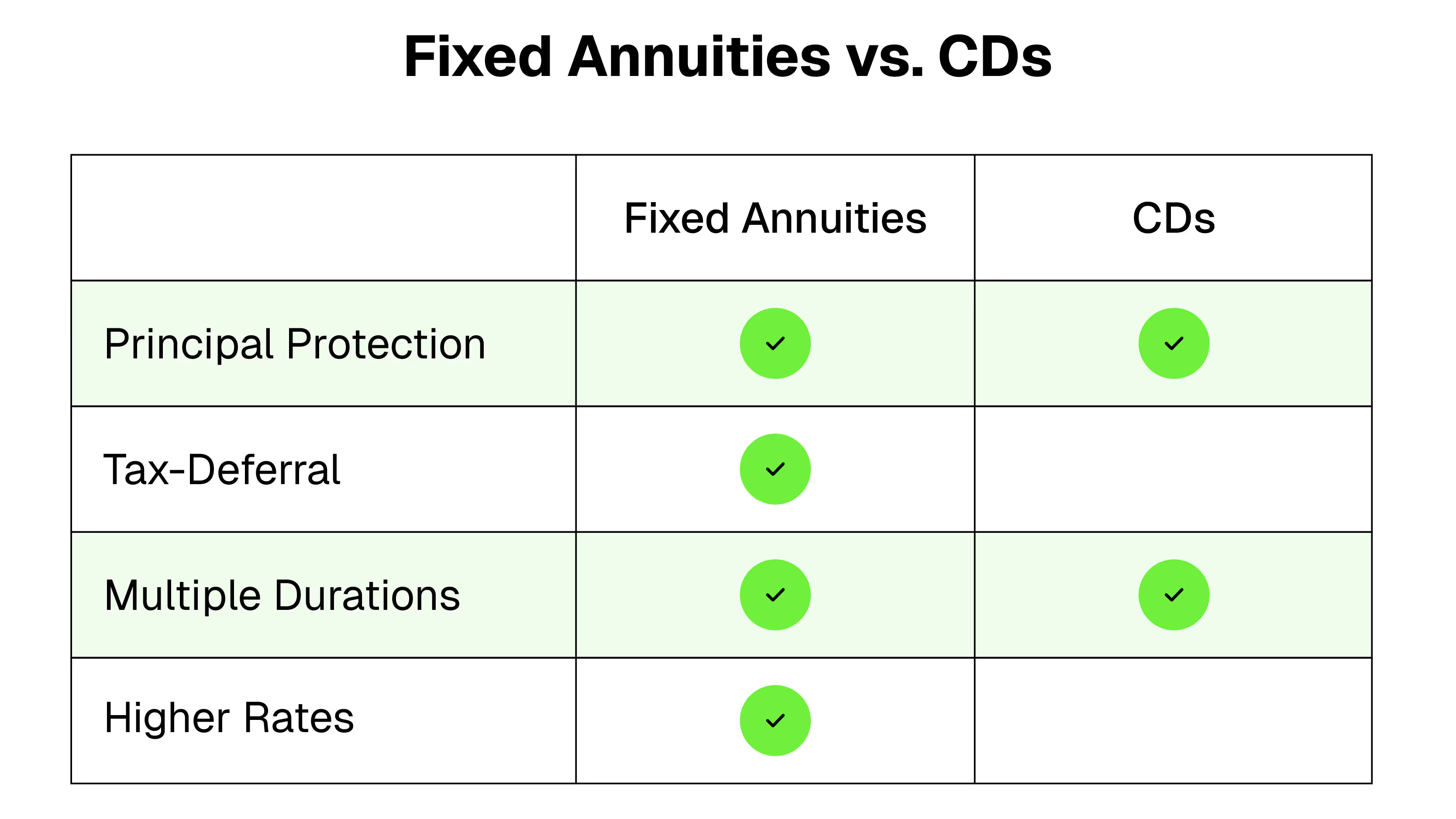

MYGAs often offer rates that are higher than those of CDs, money market funds, and short- to intermediate-term government bonds. Rates are locked in for the entire period, typically 3 to 10 years, ensuring your money works harder for you.

Worry less during volatile markets

The chance of losing assets in a market downturn makes many people uncomfortable, especially those near retirement. With a MYGA, your savings are protected from loss, and growth is guaranteed, so you can stop worrying about your retirement savings being depleted.

Provide tax advantages

Like other types of commission-free annuities, MYGAs offer tax-deferred growth. Any money that might have been paid in taxes remains in the contract, earning an attractive return. Tax-deferral means the contract accumulates value more quickly than it might otherwise.

MYGA Liquidity and Withdrawal Rules

It’s important to understand that MYGAs are not liquid assets, but many contracts allow penalty-free withdrawals up to a certain percentage of the account each year. In addition, some contracts allow all assets to be withdrawn in specific circumstances, such as a move to a nursing home. If you withdraw more than the penalty-free amount, there may be a surrender charge and potentially a tax penalty due to the IRS on interest earned if you make withdrawals before age 59½.

What Happens When a MYGA Matures?

When the annuity contract reaches its maturity date, the owner is granted full access to the principal and earnings, and has several options on how to use the funds:

- Withdraw the accumulated value

- Renew the MYGA contract at the prevailing rate

- Move the assets to another commission-free annuity

MYGAs offer a powerful way to pursue higher, guaranteed returns while protecting your principal, granting retirees peace of mind from the unpredictable nature of the market.

To learn more about MYGAs, check out the MYGA Marketplace, which features dozens of current commission-free MYGA products with a range of rates and durations from leading carriers.

[press-a-contact-location]

.avif)