Long-Term Care Planning Guide

Retirement Planning Realities

One of the biggest challenges to planning for retirement is anticipating what our health and personal care needs will be as we age. We all know that as we get older our health and ability to care for ourselves decline. But the timing and impact of these declines can be hard to predict. Many people think if they’re in good health today they’ll be able to self-manage their care needs over time.

It’s easy to underestimate future care needs, how much care will cost, and your ability to pay for it. So, planning for long-term care early — even if it’s hard to imagine needing it — is important to protect your retirement savings and ensure you have enough resources should care be needed.

The primary goal of long-term care planning is to protect your assets from costs of assisted living, nursing, or other care if you become ill or disabled.

What is long-term care and who needs it?

Long-term care refers to a range of personal and health care services provided to an individual over an extended period of time at home or in a facility.

A person typically needs long-term care when he or she is unable to do 2 of the 6 activities of daily living (ADLs) on their own. ADLs include bathing, eating, toileting, transferring, dressing, and continence. A number of situations can lead to the need for help with these and other daily activities, including an accident, an illness, or cognitive decline.

The need for long-term care can arise suddenly — after an accident or health event like a stroke — or over time due to aging or illness. Some people think their family members will be able to step in with additional care should it be needed. But, depending on the situation, care needs can quickly overwhelm what family is able to provide — physically, emotionally, and technically. The need for long-term care without a plan in place can be devastating for you, your family, and your financial stability.

Real Life Scenario:

Imagine you are in fine health as a seventy-five-year-old then one day take a nasty fall and break your hip. Suddenly and unexpectedly, you are unable to get in and out of bed on your own, dress yourself, or get up and down the stairs. You experience a long recovery and need help with these and other personal care activities until you are strong enough to resume doing them on your own. A family member helps intermittently but you require additional assistance when family cannot be with you. At $30/hour2, costs for a home aide begin to mount, and suddenly you’re looking at thousands of dollars in out-of-pocket care expenses.

This scenario is one of countless examples of when long-term care may be needed and underscores how difficult it can be to estimate your potential needs. But today there are options that help you get financial help to cover these costs.

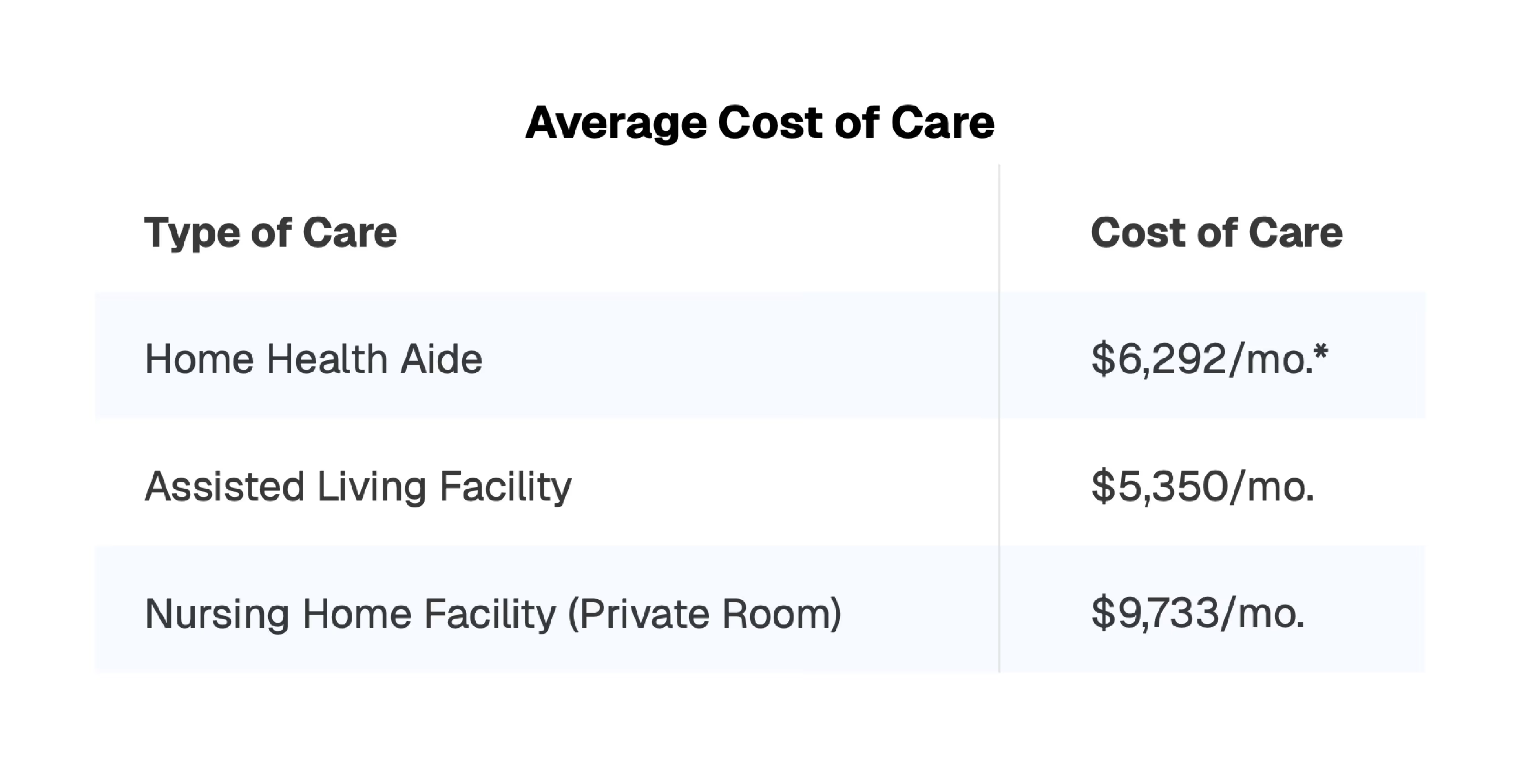

How much does long-term care cost?

Costs of care vary depending on geographic location, the care setting, type and level of care needed, and other factors. Below are some monthly median costs3 of care in different settings in the U.S., however care costs can vary greatly depending on where you are located.

People often mistakenly believe that Medicare will help pay for long-term care. Medicare, as well as most other health insurance, does not provide long-term care coverage.4

Why should I plan for long-term care when I may not need it?

You have planned for your retirement and built a nest egg to fund your desired retirement lifestyle. Long-term care planning can help protect those assets as you age and ensure you have control over your care plan. An unplanned for long-term care need could significantly deplete your savings, leaving you and/or your spouse with less to live on and less to pass on to your heirs.

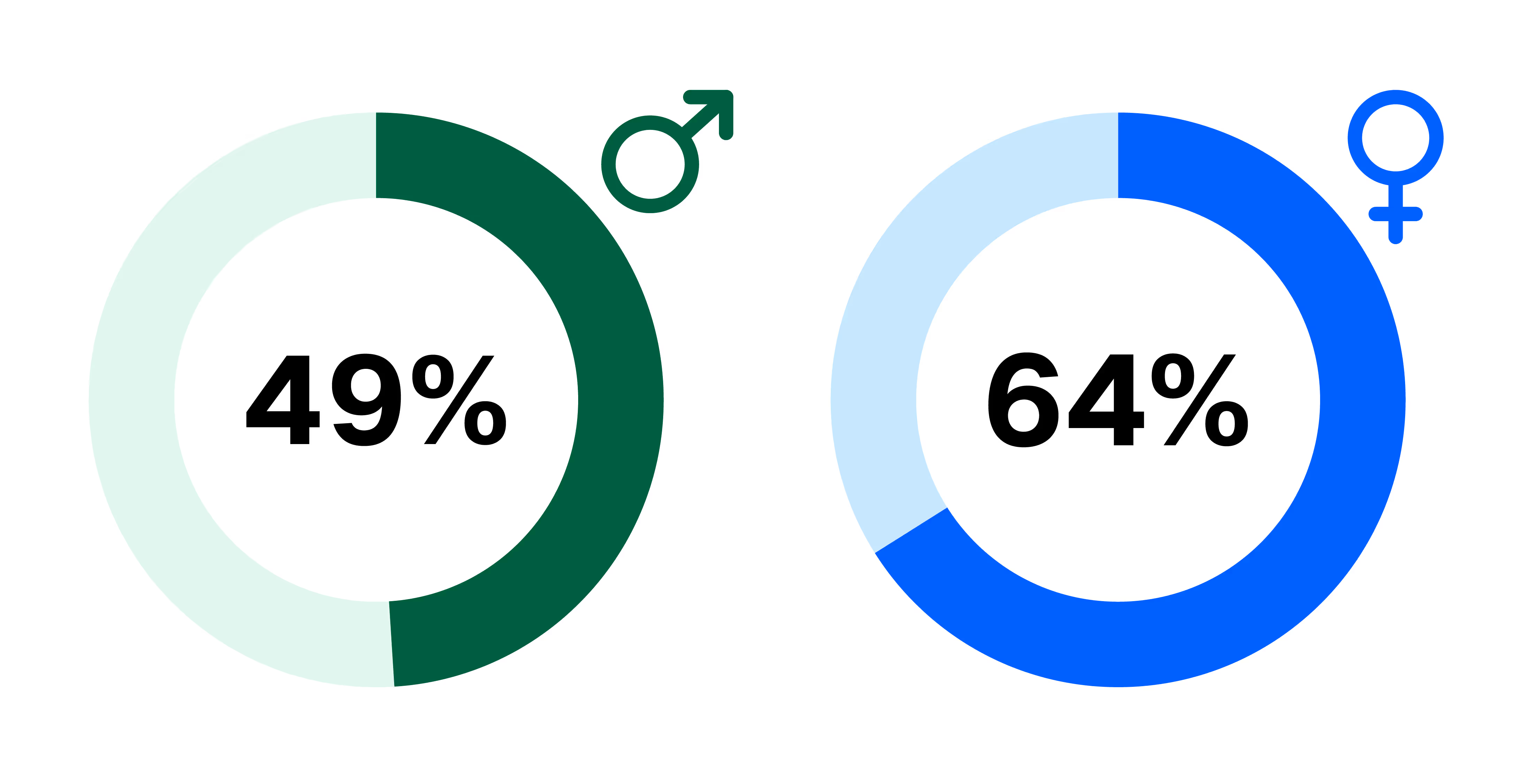

A person turning age 65 today has almost a 70% chance of needing some type of long-term care services during their remaining years. And, while one-third of today’s 65-year-olds may never need long-term care support, 20% will need it for longer than 5 years.5

What is long-term care insurance?

Long-term care insurance (LTCI) is designed to cover the costs associated with long-term care services that aren’t typically covered by traditional health insurance or Medicare. This includes assistance with daily activities like bathing or showering, dressing, getting into or out of bed, walking, eating, and using the toilet. LTCI can pay for assistance with these personal care needs over extended periods of time.

Today, you have options for long-term care insurance, including traditional and hybrid policies, as well as other types of insurance that can provide income to help pay for care expenses.

Types of long-term care insurance:

1. Traditional Long-Term Care Insurance: This is a stand-alone policy that pays for various long-term care services. Benefits are typically used for nursing home care, assisted living, home health care, or adult day care. Premiums are paid for the lifetime of the policy or until you go on claim.

2. Hybrid Policies: These combine long-term care insurance with life insurance or an annuity. They offer the benefit of long-term care coverage and, if the care isn’t needed, a death benefit or income stream. This option can be attractive if you are concerned about the possibility of not using the long-term care benefits.

3. State Partnership Programs: These are state-specific programs that coordinate with Medicaid. They allow policyholders to protect a portion of their assets while still qualifying for Medicaid if long-term care is needed.

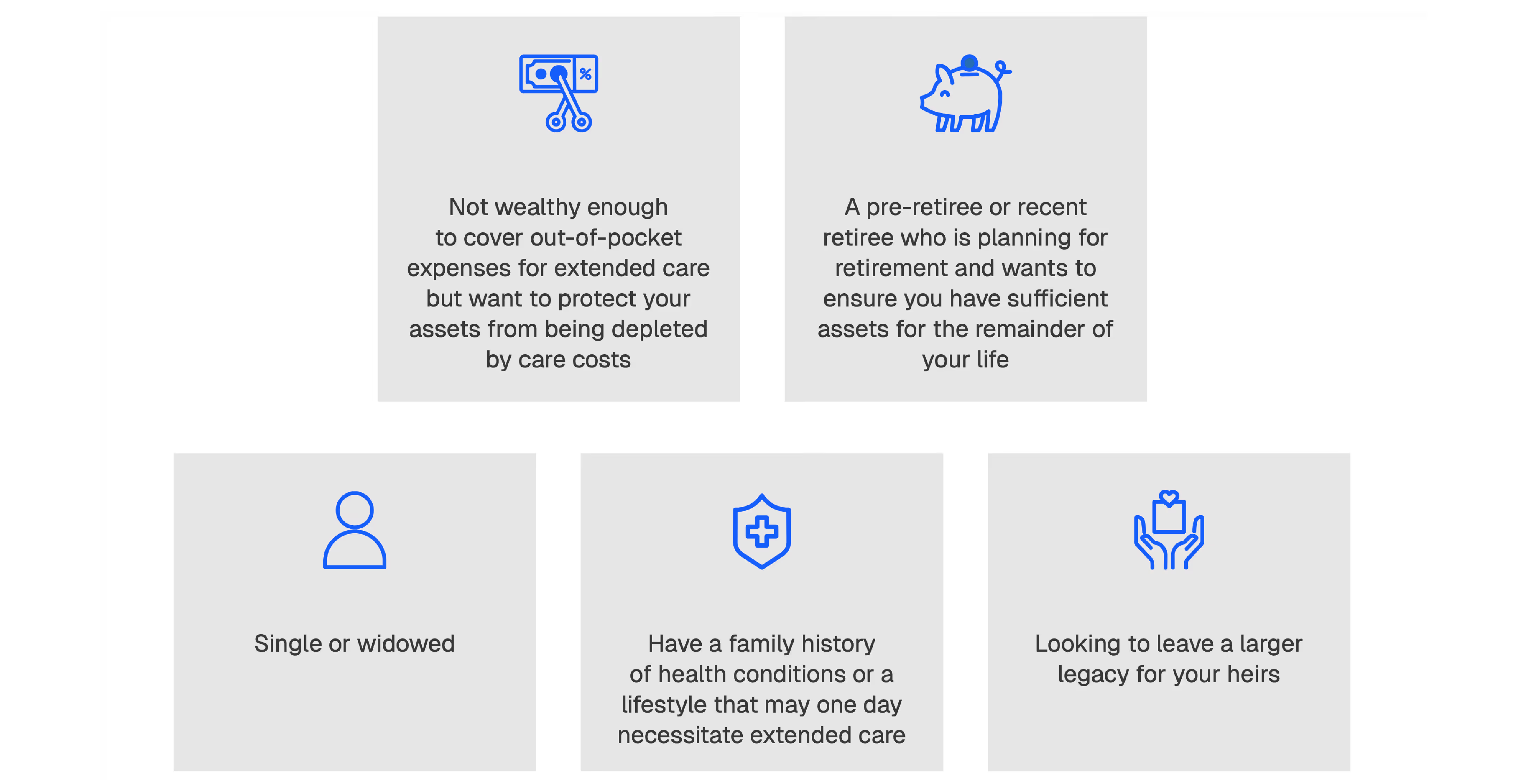

Who might need long-term care insurance?

LTCI is particularly beneficial for individuals who want to protect their financial assets against potentially high costs of care services not covered by other insurance. You should consider LTCI if you are:

When should I consider purchasing long-term care insurance?

As you age, the chances of needing long-term care increase. Timing is an important consideration when

planning for long-term care; you’ll want to have coverage before you need it. Here’s when you might want to

start:

• During Your Working Years: Purchasing LTCI during your working years can allow you to use regular income to pay premiums, rather than having to tap into your retirement income.

• In Your 50s or Early 60s: A good time to purchase LTCI is in your late 50s to early 60s. Premiums are generally lower if you buy the policy at a younger age, and you’re less likely to be experiencing health declines.

• As Part of Retirement Planning: As you approach retirement, LTCI can be a key component of your financial planning strategy to provide coverage for potential future care expenses.

• Before Significant Health Issues Arise: It’s important to apply for LTCI before any health problems develop; pre-existing conditions can make you ineligible or result in higher premiums.

What should I consider as I begin planning for long-term care?

Answers to the questions below will help guide you as you begin planning for long-term care:

1. Based on your health and family’s health history, what conditions could impact your health, and ability to care for yourself, as you age?

2. What financial resources do you have that could help pay for care assistance?

3. If you need additional personal care long-term, what resources could family or friends provide? Have you had a conversation with them about their potential role in your care?

a. Who could help take care of you and how would that work?

b. Is there anyone who could take over the management of your finances?

c. Is there anyone who could provide financial assistance?

d. If you are unable to make care decisions, who would make those decisions for you?

4. Does your family know your personal care preferences?

Real Life Scenario:

Imagine you are in your 50s and are beginning to put a long-term care plan in place. You assume your children will step in should you need financial or hands-on care assistance in the future. When you broach the subject with your children, you discover your daughter is willing and able to provide a measure of financial assistance for a short period of time. However, your son is not comfortable serving as a financial resource. He explains his children will be going to college and he is concerned about funding their tuition and having reserves for unexpected family needs.

This scenario exemplifies the planning conversations you will need to have with family and others to clarify who will provide future assistance, what type and how much. It’s important to have these conversations in advance to give everyone time to consider and agree to their potential role.

Common misconceptions about long-term care

1. I’m in good health and won’t need long-term care.

About 70% of people who are 65 today will need some form of care4 and an event requiring long-term care can happen at any time.

2. Medicare will cover my long-term care costs.

Medicare typically does not cover long-term care or provides limited coverage. Learn more aboutMedicare coverage.

3. My family will provide care should I need it.

While family members may want to help with your care needs, sometimes care requires more skills or time than family members can provide.

4. Long-term care is only for end-of-life.

Long-term care can include but is not limited to end-of-life care. LTC encompasses personal care assistance due to chronic illness, physical disabilities, cognitive impairments and recovery/rehabilitation from surgery or illness.

5. Long-term care insurance is too expensive.

There are different types of coverage for long-term care expenses and costs will vary based on factors like your gender, age, health status, and type of coverage.

Next Steps

Having a long-term care plan in place before care is needed can provide peace of mind that your retirement assets are protected, and that you’ll have resources to cover costs of extended care in the event you need it. Talk to your financial advisor to learn more about options available to you for long-term care coverage and what to consider as you prepare your plan.

If you do not have a financial advisor and are interested in being connected with one, we can help. Call us at 877.625.5544.

[press-a-contact-location]

Sources:

1 Department of Health and Human Services (HHS)

2 Based on industry estimate for professional in-home caregivers

3 Genworth

4 Medicare.gov

5 LongTermCare.gov

6 Forbes

Disclosures:

* Based on industry estimate of 44 hours per week for professional in-home caregivers

• Not a deposit • Not FDIC or NCUSIF insured • Not guaranteed by the institution • Not insured by any federal government agency • May lose value

All guarantees are based on the financial strength and claims-paying ability of the issuing insurance company.

© 2025 DPL Financial Partners, LLC. All rights reserved.

.avif)