Retirement Income Planning Guide

Today’s Retirement Realities

Retirement can be wonderful time in life when it’s possible to spend more time with family and friends, pursue hobbies, travel, and relax after decades of hard work. But planning for retirement, and ensuring

you’ll have enough money to fund your spending needs, can be challenging.

Part of the challenge comes from all the retirement unknowns — How long will I live? Will I stay healthy? What will the markets do?

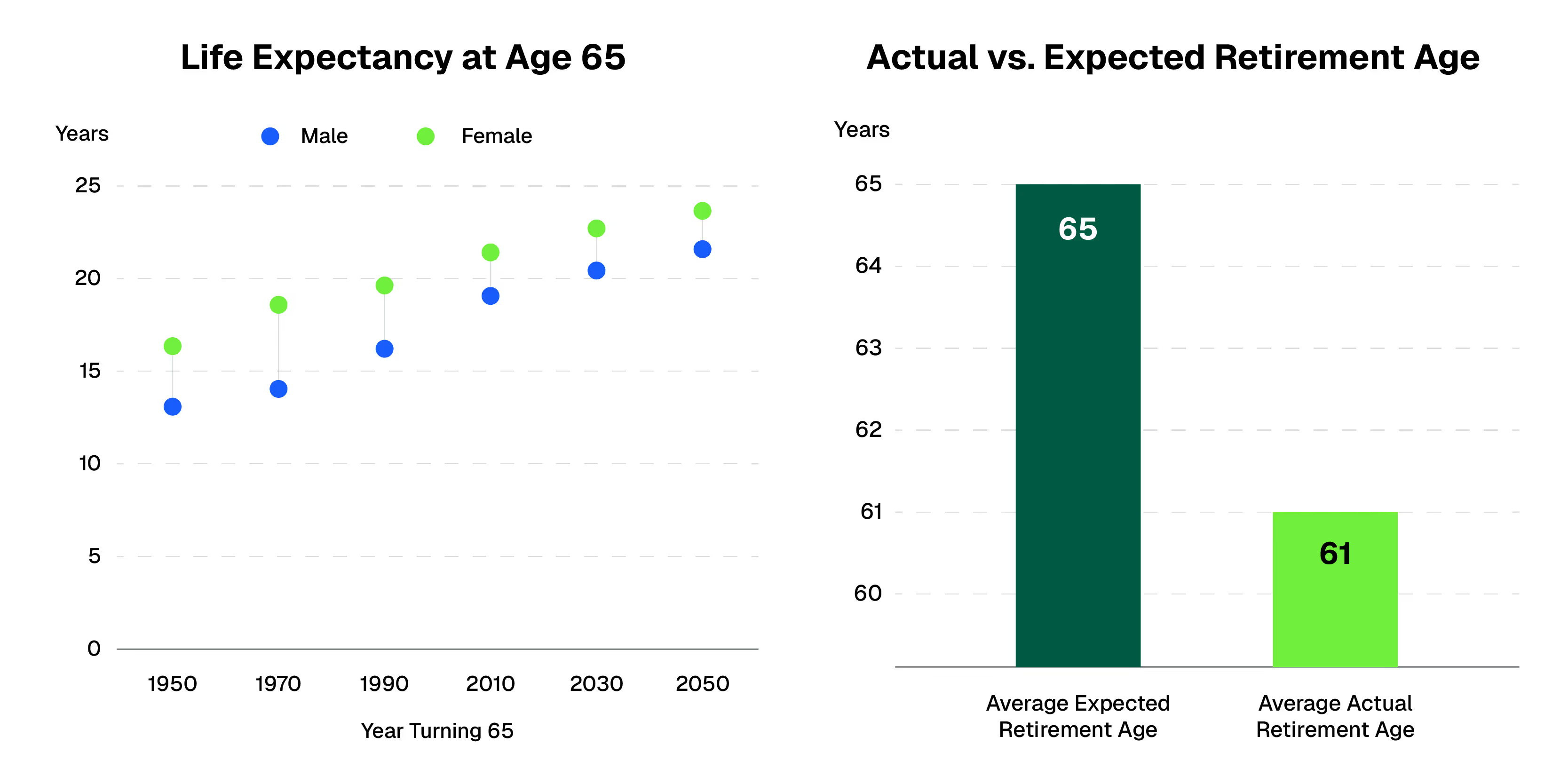

Retirement looks different today than it used to. When Social Security was established in 1935, just over half of Americans lived to age 65, and retirement averaged 13 years.1

Today Americans are living longer, and retiring earlier.2 Modern retirements can span 30 years or more!

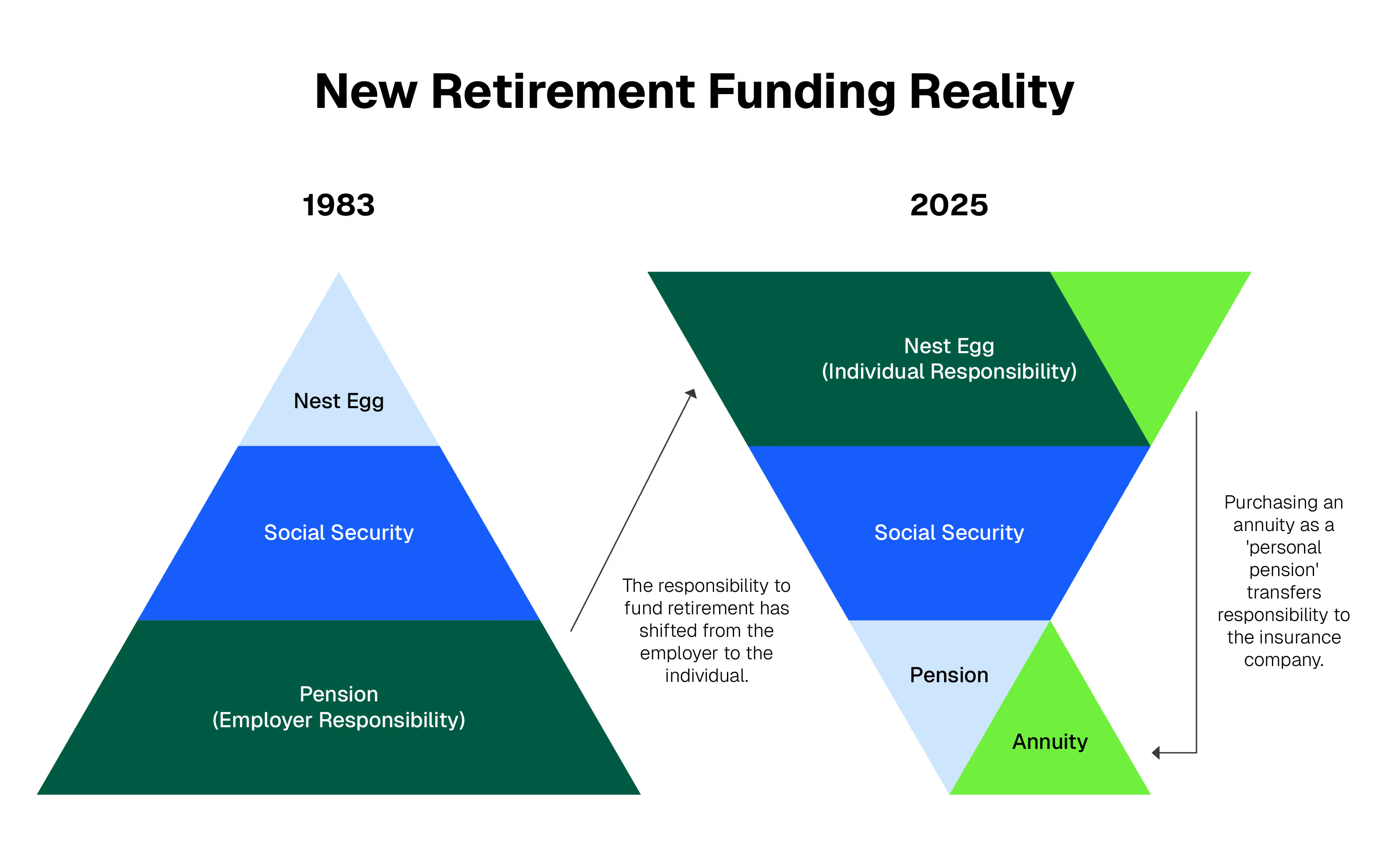

The options for funding retirement have changed too. Traditional pensions, and the reliable retirement paychecks they provide, are disappearing. The burden of turning retirement savings into guaranteed income has transitioned from employers to retirees.

Given these new realities, retirement planning and guaranteed income have never been more important.

Addressing the Two Greatest Risks in Retirement

Understanding risks that can derail a retirement is key to creating a successful income plan. Two of the greatest risks are longevity risk and sequence of returns risk.

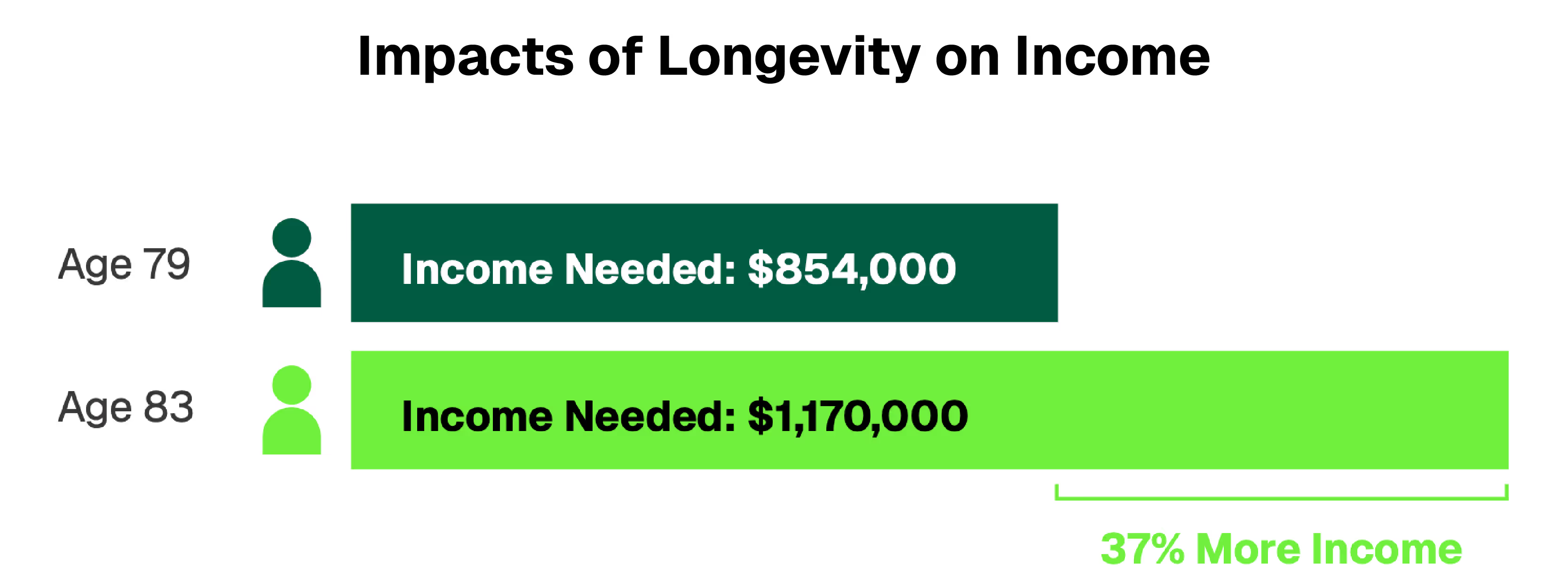

Longevity risk is the risk that you will outlive your retirement income and no longer be able to fund your living expenses.

Here is an example of what living longer can mean for your income requirements: A 65-year-old living 14 years to age 79 would need $854,000 in income to meet his or her expenses. By living an additional four years to age 83, the total retirement income need increases to $1,170,000 — 37% higher — assuming 3% inflation.5

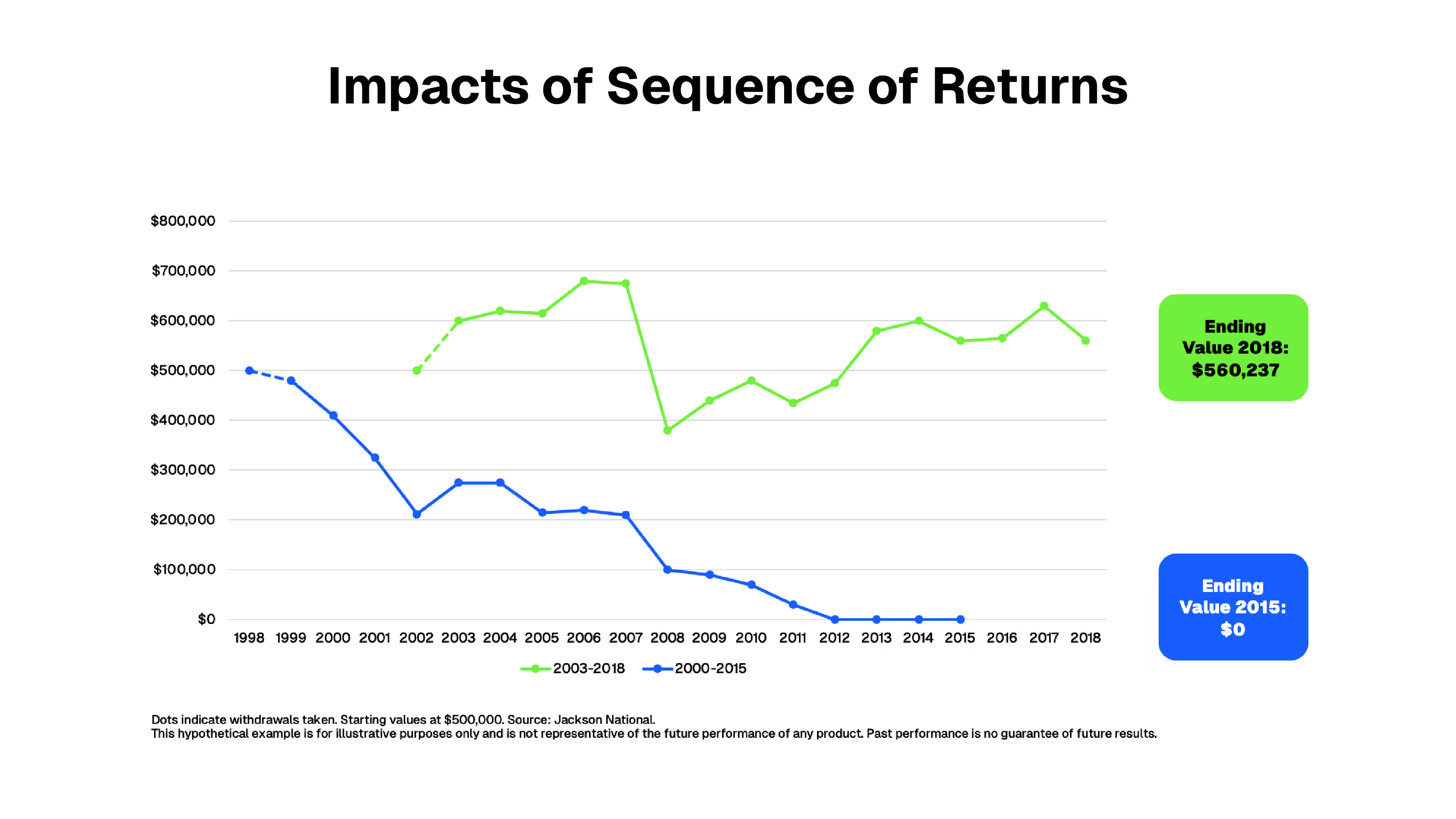

Sequence of returns risk is the risk that a market downturn just before or soon after you retire depletes your portfolio to the point it is unable to support income withdrawals throughout retirement. This can be devastating for individuals who rely on their investments to fund their retirement spending.

Example: Two people with identical portfolios retire four years apart. Portfolio 2 experiences a market downturn soon after retirement and the start of income withdrawals; Portfolio 1 experiences an up market. Portfolio 2 is unable to recover as withdrawals deplete a proportionally smaller account.

There are other risks as well, including overspending early in retirement, which can put pressure on your portfolio and potentially reduce future income. A well-thought-out retirement plan will help mitigate these and other risks by protecting a portion of your assets, needed for income, from market volatility, and ensuring you will have enough protected income to cover at least your essential expenses for as long as you live, no matter how long that may be.

Retirement Income Planning

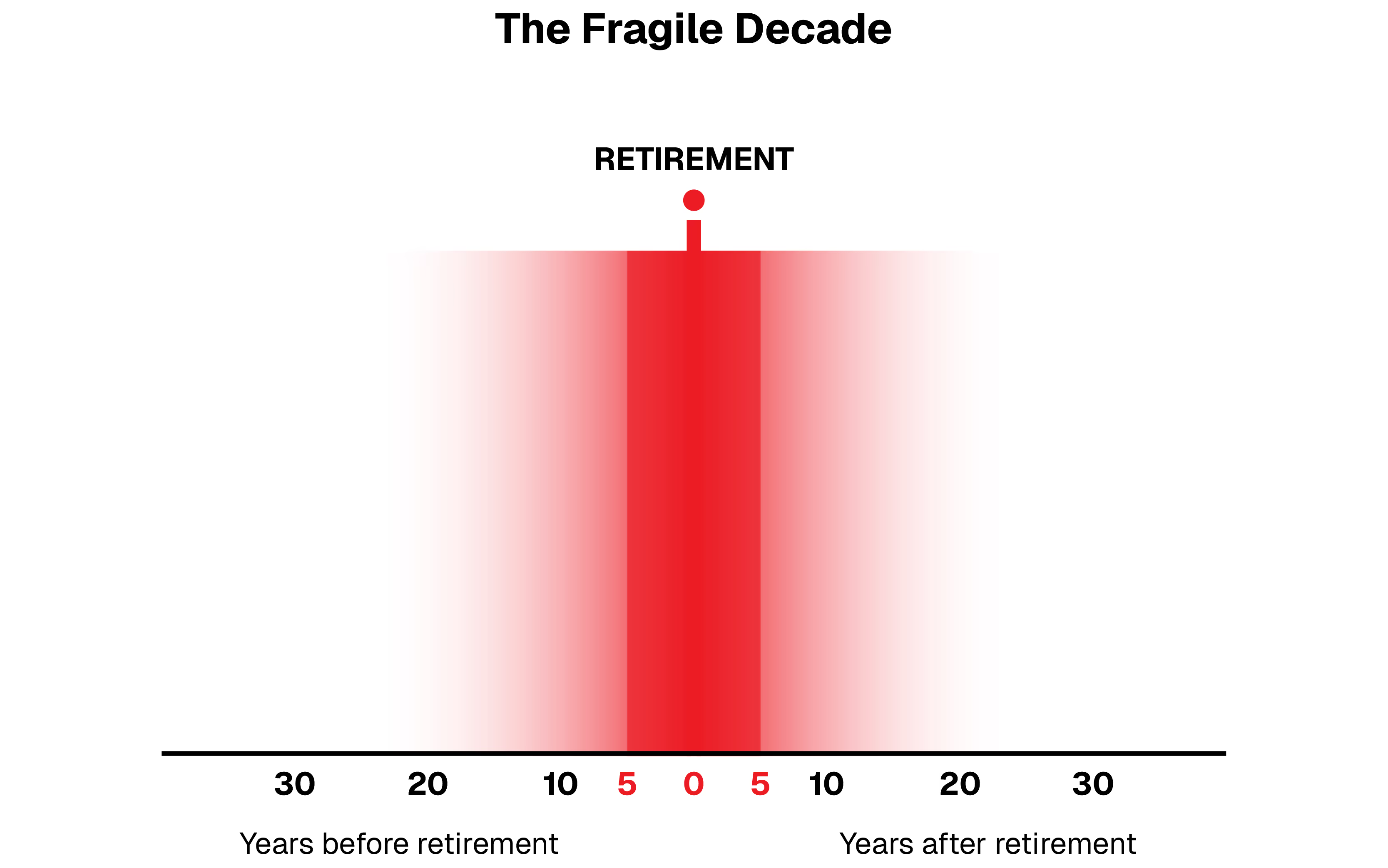

One of the keys to a successful retirement is to start planning early. The five years before and five years after retirement are referred to as “the fragile decade” because 80% of a successful retirement outcome is determined during this critical timeframe.6

Waiting too long to begin planning can expose you to risks. You may be forced into retirement earlier than you expect, by a health event or corporate downsizing, without a plan in place. Or, a market downturn could negatively impact your investment portfolio and future income if you haven’t prepared.

And, understand that people’s financial goals and tolerance for risk often change once they retire. Investment strategies that worked to build wealth may not be appropriate — financially or emotionally once you begin “decumulating” your assets to fund retirement spending.

A planning process that considers all the tools available to address these challenges helps you determine the retirement income strategy that’s right for you.

Power of Guaranteed Income

Guaranteed income can be a powerful tool in a retirement plan, providing a predictable and secure stream of income, and peace of mind that you’ll have funds you can count on no matter when you retire, how long you live, or how the markets perform.

Three primary sources of guaranteed income for retirees are Social Security, pensions, and annuities. Annuities are insurance products designed to provide guaranteed lifetime income.

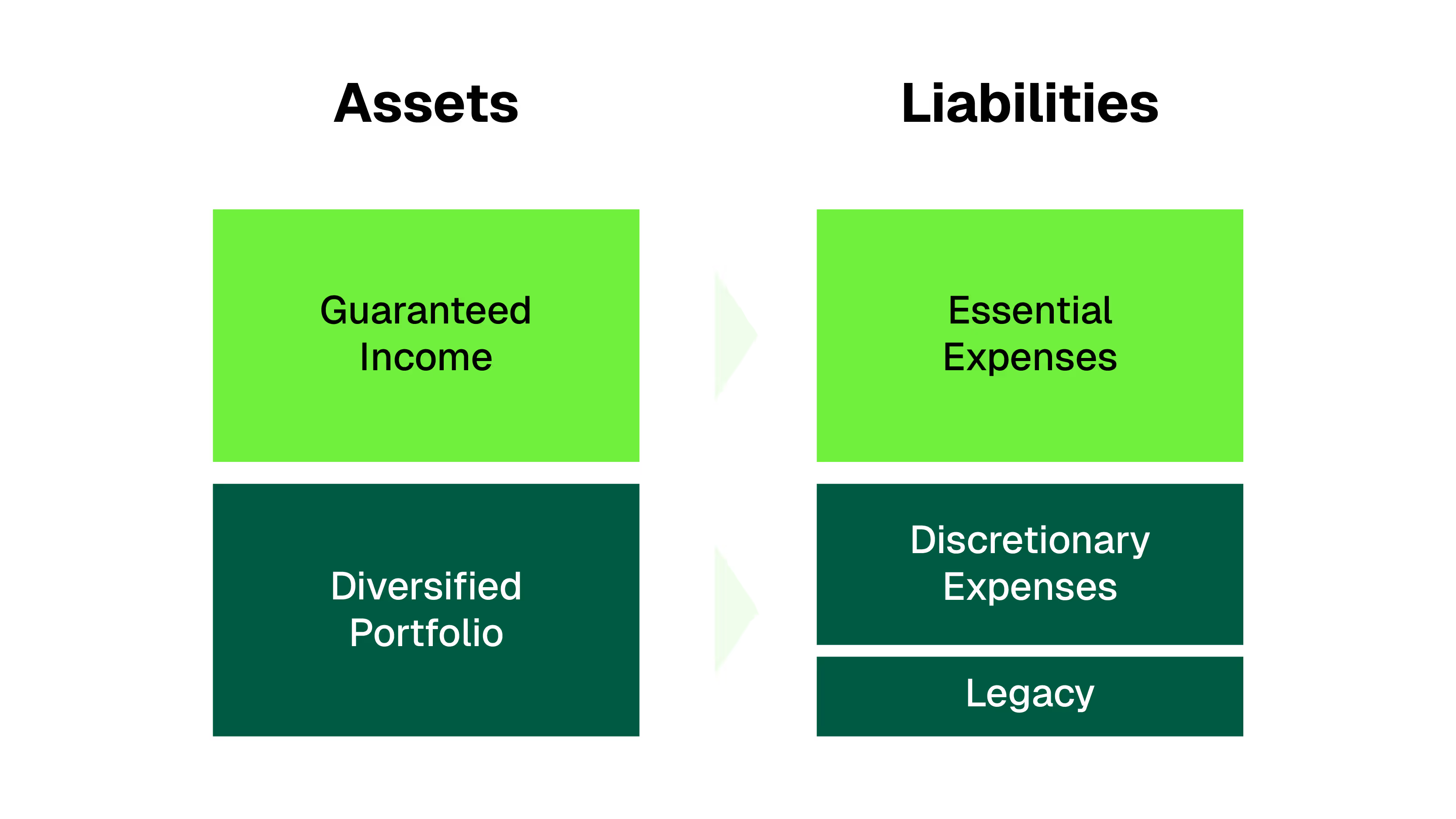

Income from annuities often is used to cover living expenses in retirement, ensuring essential costs are covered and providing flexibility to invest the rest of the portfolio more aggressively for growth and discretionary spending.

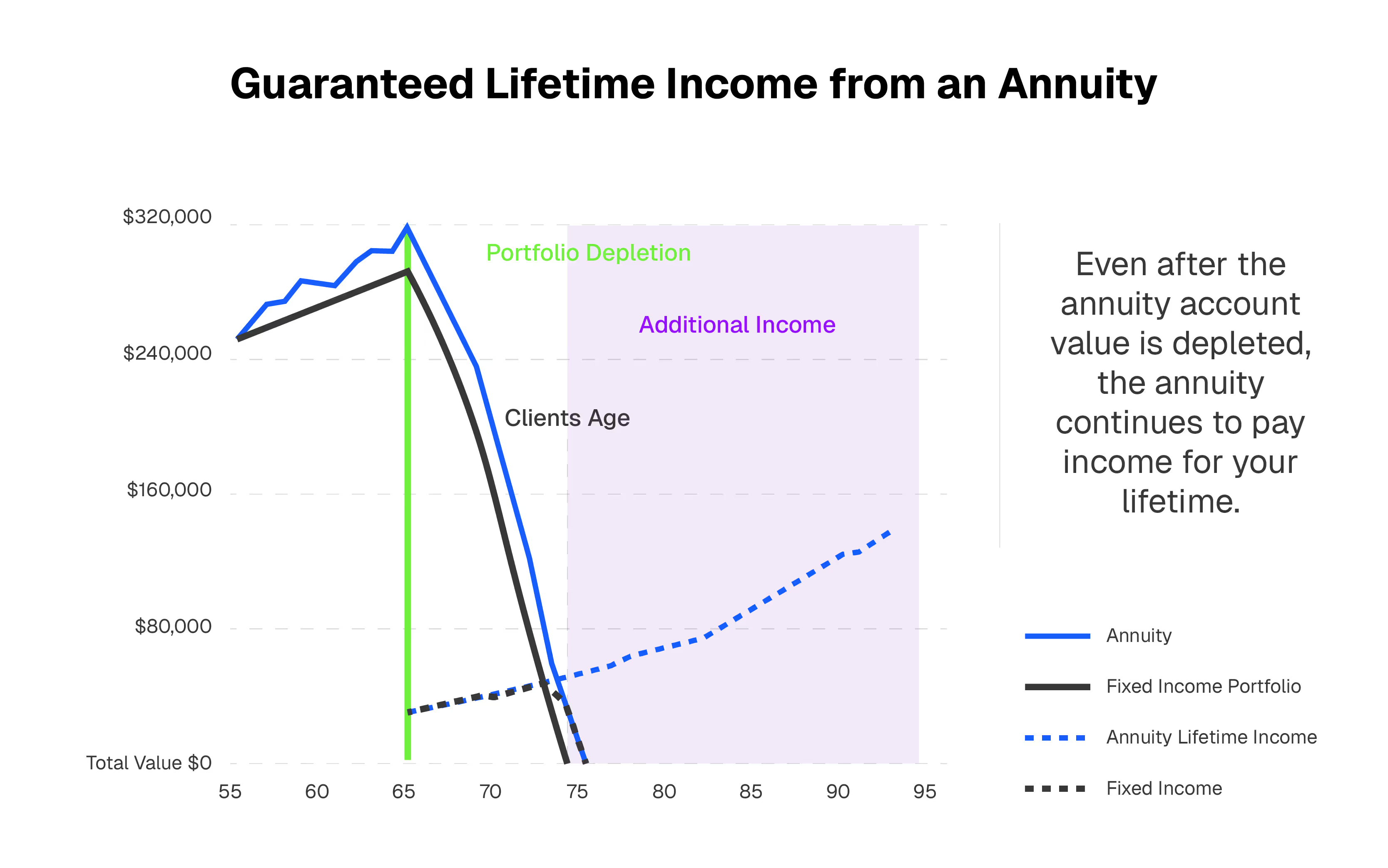

Modern, commission-free annuities can potentially generate income more efficiently than bonds, and guaranteed income payments can continue even after the account is depleted, lasting for as long as you live.

Considering these benefits, it’s no wonder people protected by guaranteed lifetime income from an annuity have a significantly more positive outlook on their retirement prospects.7 This helps explain why annuity sales have surged in the last few years.8 Learn more about guaranteed income.

Identifying How Much Income You’ll Need

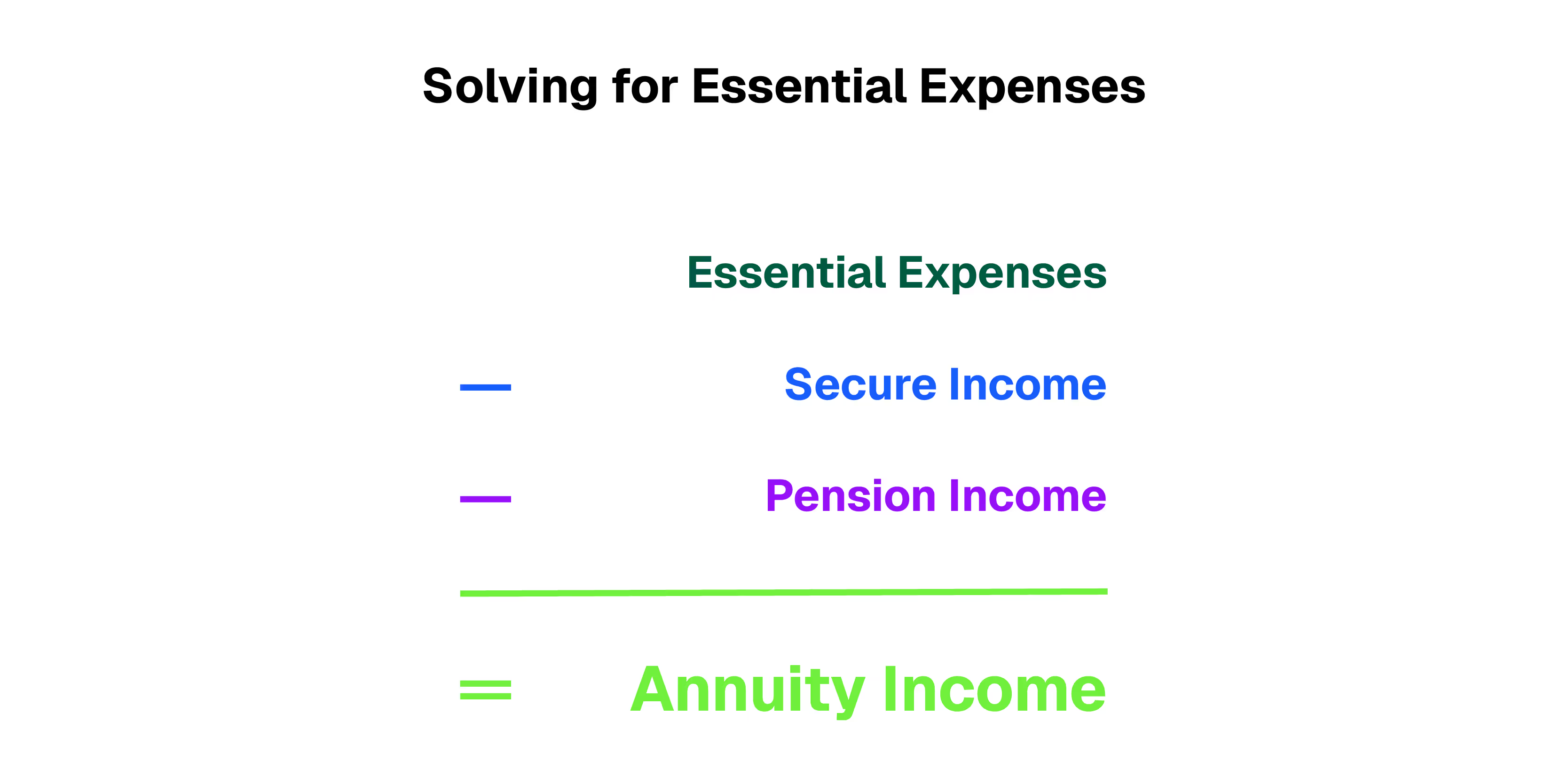

When considering how much income you’ll need in retirement and the best way to generate it, a good place to start is by determining how much your living expenses will be after you retire, like housing, food, clothing, etc. Guaranteed income from an annuity is often used to help fund these costs, giving you peace of mind that you’ll have money to meet your essential needs no matter how long you live.

By adding up your anticipated living expenses, then subtracting anticipated income from other secure sources like Social Security and/or a pension, you can arrive at the income gap to fill with an annuity. You then can determine how much money you would need to put into an annuity and what type of annuity is best suited to meet the income need.

And, with your essential expenses covered by guaranteed income, the rest of your portfolio can be invested to fund discretionary spending and a legacy, if that is a goal.

Social Security is a key source of retirement income for Americans. Since the government offers inflation adjustments, getting the highest benefit from the start is a smart move. Delaying your Social Security benefit until age 70 can increase your lifetime payout significantly.9 Consider building a retirement income bridge using an annuity to maximize your Social Security income.

Learn more about building an income bridge to maximize your Social Security lifetime benefit.

Understanding What Modern Annuities Can Do

In the past several years, annuities have changed. Traditional annuities are commission-based, meaning a salesperson is paid a commission to sell the products. Commissions drive up product costs, add complexity, and can erode benefits.

Modern annuities are commission-free and offer lower costs, greater transparency, and improved benefits to consumers. These simplified products are built to deliver better value and a buying experience you control, vs. a sales process a salesperson controls.

It is important to understand that there are many types of annuities, each with distinct features and benefits. Some annuities provide complete asset protection while others offer partial protection with greater growth potential.

There are annuities designed to start paying income immediately, and others designed to grow your money before paying income at a date of your choosing in the future.

And, some annuities offer income options that include a cost-of-living adjustment (COLA), which can help offset the impacts of inflation on purchasing power over the course of your retirement.

You have many options; the right annuity will be determined by your needs.

Read about the most common annuity misconceptions.

How to Fund an Annuity

When considering an annuity for retirement income, think of it as an alternative to fixed income.

Commission-free annuities can potentially generate income more efficiently than fixed income, meaning it costs less to fund an income need using an annuity than a bond, for example. So funding the annuity from a portion of your bond allocation can be a smart strategy.

“Bonds are the least efficient way to fund retirement spending...An annuity is a more effective bond. Its going to provide a fixed income approach that is linked to the needs of the individual.”

– Wade Pfau, PhD | Professor of Retirement Income at The American College of Financial Services

Other sources include assets from a 401k or IRA, and cash. Keep in mind, once you reach 59.5 years-old, you may be able to withdraw money from your 401k tax-free, depending on your plan and personal circumstance. Using accumulated retirement savings to fund an annuity can be a smart way to create a stream of guaranteed lifetime income. Think of this as creating a personal pension.

How you fund an annuity for retirement income will depend on how and where your assets are invested at the time of purchase.

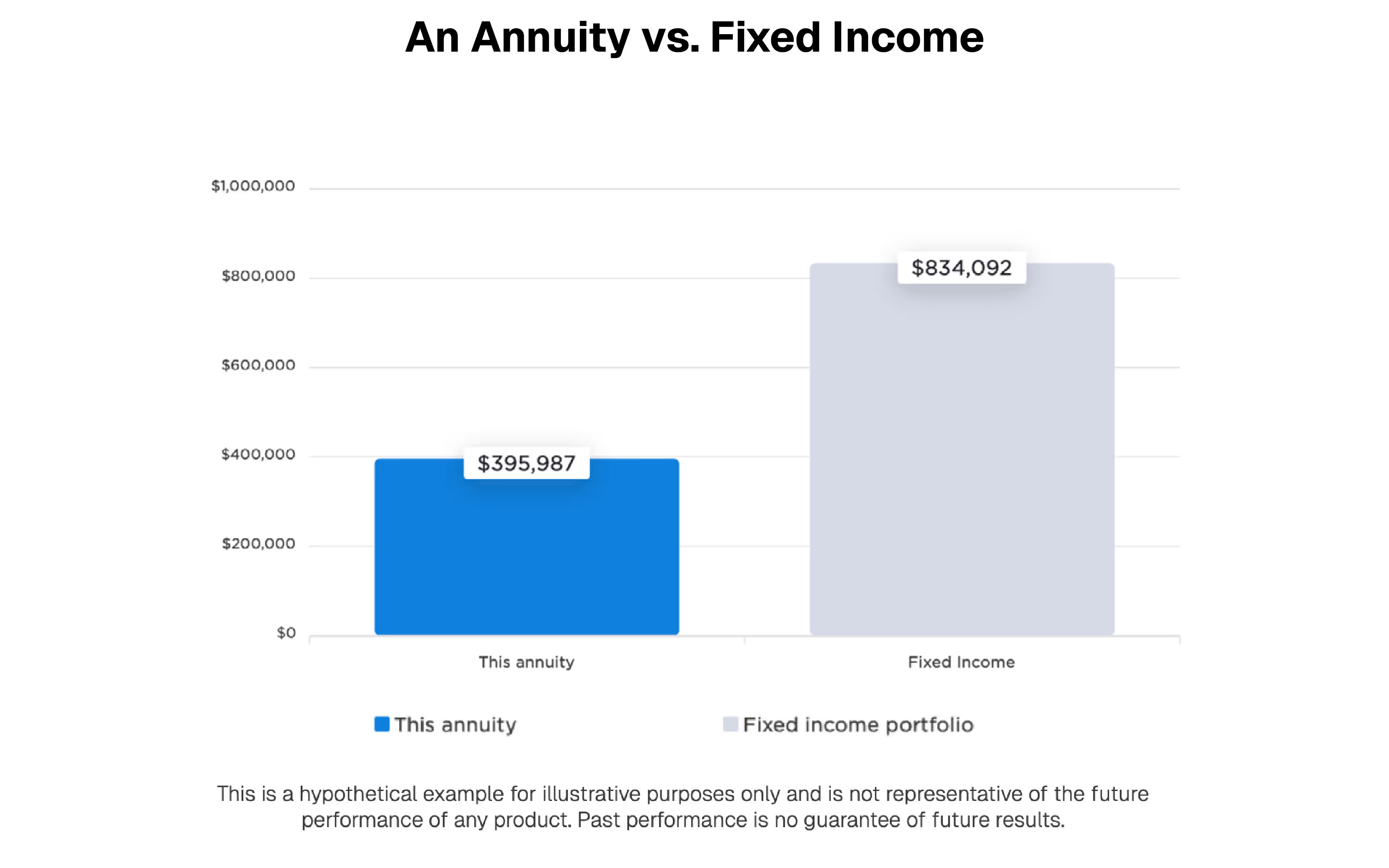

Example: An annuity can potentially generate income more efficiently than a fixed income portfolio. DPL’s Fixed Income Comparison tool (see below) illustrates the cost of funding a $5,000 per month income need with an annuity returning 6.51%, versus fixed income, assuming a 5% fixed income return.

Learn more about using annuities in a financial plan.

Next Steps

Annuities are powerful tools that are uniquely designed to generate guaranteed income for retirement. And, now, modern annuities are available without commissions from many leading insurance carriers, offering lower costs and improved benefits.

There are many types of annuities, and it’s important to work with your financial advisor to determine if an annuity fits into your retirement income plan and which product is right for you. We can help.

[press-a-contact-location]

Sources:

1 https://www.ssa.gov/history/lifeexpect.html

2 https://finance.yahoo.com/news/jaw-dropping-stats-state-retirement-200025720.html

4 Morningstar

5 https://www.irionline.org/research/article/iri-fact-book-2023/?ysso_log_in=true&Site=iri)

6 Wade Pfau, Retirement Planning Guidebook

7 ALI Cannex Protected Retirement Income & Planning (PRIP), https://www.limraconsumer.com/wp-content/uploads/2023/06/Press-Release-PRIP-2023-Consumer-FINAL-061423.pdf

9 Social Security Administration

Dicslosures:

Guarantees are based on the claims paying ability of the insurance carrier issuing the product.

• Not a deposit • Not FDIC or NCUSIF insured • Not guaranteed by the institution • Not insured by any federal government agency • May lose value

When evaluating the purchase of a variable annuity, you should be aware that variable annuities are long-term investment vehicles designed for retirement purposes and will fluctuate in value; annuities have limitations; and investing involves market risk, including possible loss of principal.

The general distributor for variable products is Johnstone Brokerage Services ("JBS"), member FINRA/SIPC 117 San Augustine Street, Center TX 75935. JBS is wholly owned by DPL Financial Partners

Fixed index annuities are not stock market investments and do not directly participate in any equity, bond, other security, or commodities investments. Unless stated otherwise, market Indices do not include dividends paid on the underlying stocks, and therefore do not reflect the total return of the underlying stocks; neither an index nor any market index annuity is comparable to a direct investment in the equity markets. Clients who purchase index annuities are not directly investing in a stock market index.

This material is not a recommendation to buy or sell a financial product or to adopt an investment strategy. Investors should discuss their specific situation with their financial professional.

© 2025 DPL Financial Partners, LLC. All rights reserved.

.avif)