Thinking About Purchasing an Annuity? Consider the ‘Cost of Waiting’

When the Federal Reserve raised its benchmark rate 11 times between 2022 and 2023 to fight inflation, interest rates on annuities climbed to historic highs. Annuity sales soared as many people took action to lock in the strong rates and other benefits by purchasing simple, fixed annuities.

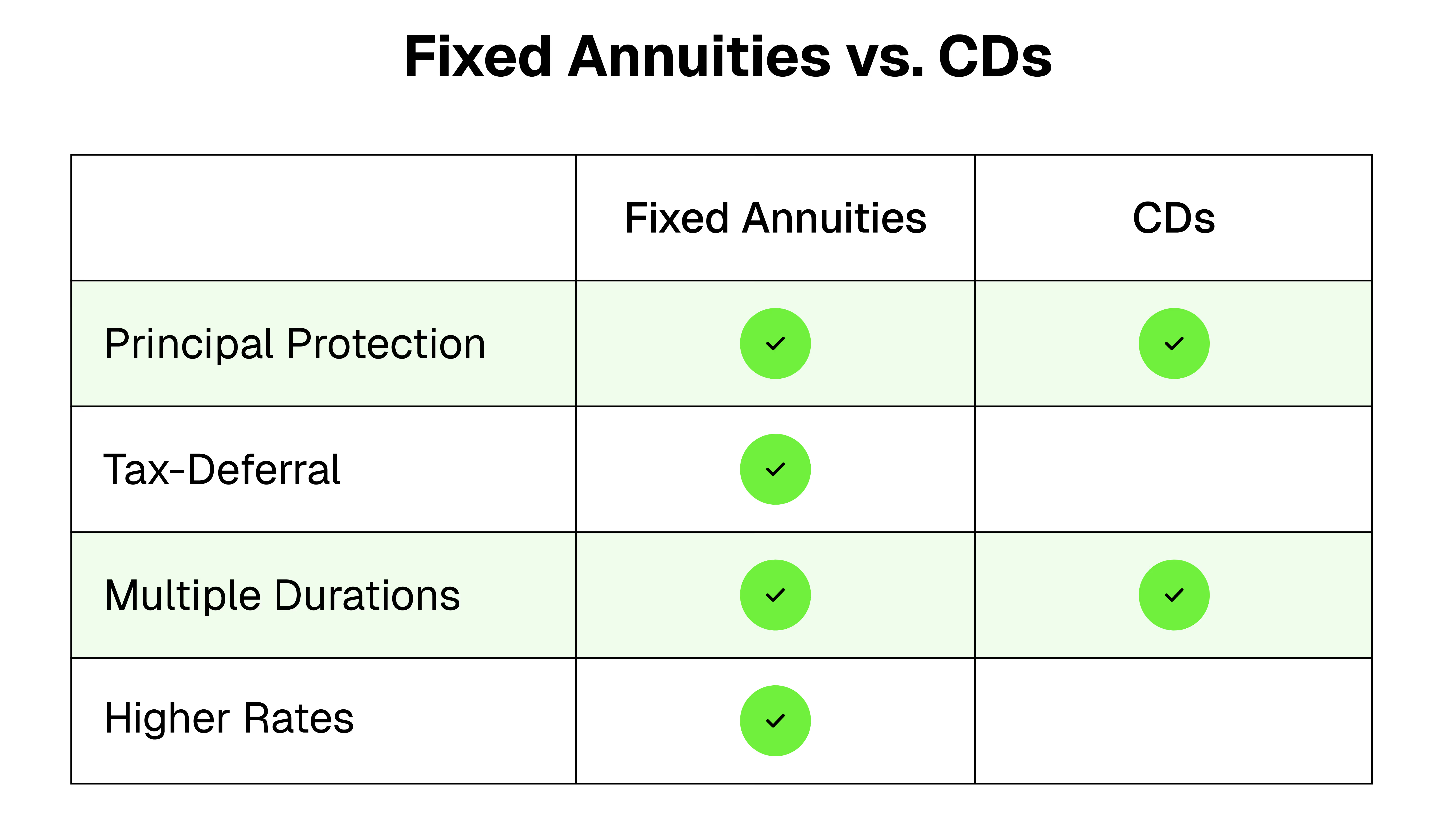

Interest Rates and Fixed Annuities

Fixed annuities are popular because they offer a guaranteed interest rate and low risk to the investor.

One type of fixed annuity, called a multi-year guaranteed annuity (MYGA), often offers higher rates than comparable certificates of deposit (CDs), as well as:

• Guaranteed returns over a specific period, ranging from 2 to 10 years

• Tax-deferred growth

• Principal protection

• Access to a portion of your funds while still keeping your rate

The rates currently available on fixed annuities (and CDs and bonds) could move lower with the Federal Reserve’s interest rate cuts and further cuts possible before the end of the year.1 So, now is a good time to secure a good rate and lock in guaranteed returns for the future.

“Now is a good time to secure strong annuity rates and lock in guaranteed returns.”

See current rates on commission-free MYGAs.

The Cost of Waiting

Some investors hope rates will rise again before purchasing. But history shows that waiting can be costly:

- When the Fed cut short term rates to below 2.5% in the spring of 2008, it held them below that level for the next thirteen-and-a-half years

- Investors who delayed purchases lost significant income opportunities during that time

“When the Fed cut rates below 2.5% in 2008, rates stayed under that level for 13+ years.”

People who opt to wait may experience what is known as “the cost of waiting.” That cost is the amount of interest an investor loses by delaying their purchase until after rates have moved lower (having hoped rates would move higher).

Is a MYGA Right for You?

MYGAs offer a range of benefits to investors that are not impacted by interest rates, including a guaranteed stream of income for retirement and protection from market volatility.

And, unlike CDs or money market funds, assets in a MYGA grow tax deferred, which means you can use non-qualified and qualified (IRA) funds, allowing for the possibility of greater accumulation over the life of the product.

MYGAs can be a good option if you:

• Are nearing or in retirement

• Are looking to protect some assets from potential market downturns

• Want to earn a better return on cash long term.

Explore Your Options

Today, low-cost, commission-free MYGAs and other types of annuities are available that can provide guaranteed lifetime income, tax-deferred growth, asset protection, and other meaningful benefits as part of your financial plan.

These modern annuities are less expensive and less complex than the traditional, commissioned annuities that preceded them.

Now is a good time to explore your options. Learn more about how to harness the power of annuities in your financial plan.

[press-a-contact-location]

Before purchasing an annuity, it is important to compare product types, benefits, and costs to ensure the product you select is suitable for your goals and needs.

Learn more about how interest rates impact annuities and whether and when an annuity is right for you.

1 CNBC

.avif)